For high-net-worth investors fearful of market volatility, managing market risk might require more than simply increasing bond allocations or reducing equity exposure. In addition to going to bonds and structured notes, there are other options, including Lido’s proprietary Cap & Cushion strategy, which offers a way to remain invested in, or become invested in, equity markets, participate in the upside up to a defined level, and receive meaningful downside protection.

This Insight explains how Cap & Cushion works, why Lido developed it, how it compares to structured notes, and when it may be appropriate as part of a broader wealth management strategy.

Exploring Options Beyond Traditional Defenses

Most investors instinctively reach for bonds when they want to reduce risk. They reason that bonds historically provide income and tend to hold value when equities decline. But in practice, a large allocation to fixed income trades one set of risks for another. It reduces the portfolio’s long-term growth potential, introduces interest-rate sensitivity, and, in low-yield or high-inflation environments, may not provide adequate income to meet spending needs.

Structured notes, offered by major banks, emerged as an alternative. They introduced to investors the opportunity to participate in market upside up to a cap, with downside protection built in. Similar products also emerged in the annuity space through Registered Index-Linked Annuities (RILAs).

Lido studied these products extensively, beginning around the 2016 election cycle, a period of genuine uncertainty that made downside protection attractive. However, the fees embedded in these products meant this protection could come at a high cost. These products are also notoriously illiquid. Investors who need to exit early often do so at a significant discount if they can exit them at all. And there is counterparty risk associated with the product’s issuers, unlike in exchange-traded securities.

We concluded that the concept was sound, but the execution, as delivered by banks and insurance companies, was unnecessarily costly, since it could be recreated directly in client accounts. So, believing fees to be the enemy of performance, Lido built the same protection differently.

How Cap & Cushion Works

Cap & Cushion is a strategy built from exchange-traded options and ETFs, constructed directly inside each client’s investment account. There is no bank intermediary, no third-party product fee, and no lockup. A version of Cap & Cushion that uses ETFs tracks a major equity index, most commonly the S&P 500® index, over a defined period, typically around one year. And because these securities are constructed directly in client accounts, we can tailor the strategy to an individual investor’s goals and objectives, rather than a single outcome chosen in a structured note or annuity product.

The core mechanics involve five components:

Buying the index ETF at the current price, which provides upside participation in the index.

Buy the right to sell at the current price by buying a put option, which provides downside protection.

Agree to sell away your upside past a defined level through selling a call (for example, 10–15% above the current market).

Agree to buy back into the index’s downside past a defined floor by selling a put. (for example, 15–20% below the current market)

Use the future anticipated dividends of the index ETF, along with the premiums from selling the call and the put, to pay for the cost of buying the put, and therefore the protection. If you’re not deeply familiar with options, the following definitions will help ground the mechanics mentioned above.

An exchange-traded option is a standardized, transparent contract granting the holder the right, but not the obligation, to buy or sell an underlying asset at a predetermined price by a specified date. They are listed on regulated exchanges such as the Cboe and overseen by the SEC.

Call Option

A call option gives the holder the right, but not the obligation, to buy a security at a predetermined price (called the strike price) on or before a specific date. When an investor buys a call, they benefit if the underlying security rises above the strike price. When an investor sells a call, they collect a premium upfront but agree to cap their participation in upside gains beyond the strike price. Buying an option is sometimes called “going long;” selling an option is sometimes called “going short.”

Put Option

A put option gives the holder the right, but not the obligation, to sell a security at a predetermined price on or before a specific date. When an investor buys a put, they gain protection if the underlying security falls below the strike price. When an investor sells a put, they collect a premium but agree to absorb losses if the underlying falls below that strike.

Premium

The price paid or received for an options contract. In the Cap & Cushion structure, premiums collected from selling options can help offset the cost of buying options.

All of the derivative pieces have the same expiration date. The result is a defined-outcome structure over a set period of time. You know in advance the level of upside participation you are targeting and the level of protection you will receive in a downturn over that time period. Positions are actively managed as market prices change and options approach their expiration dates. And the derivatives and ETFs are liquid, so positions can generally be adjusted or unwound prior to expiration, either to raise cash, systematically rebalance, or take advantage of new market conditions. However, doing so may affect the realized outcome of the defined structure.

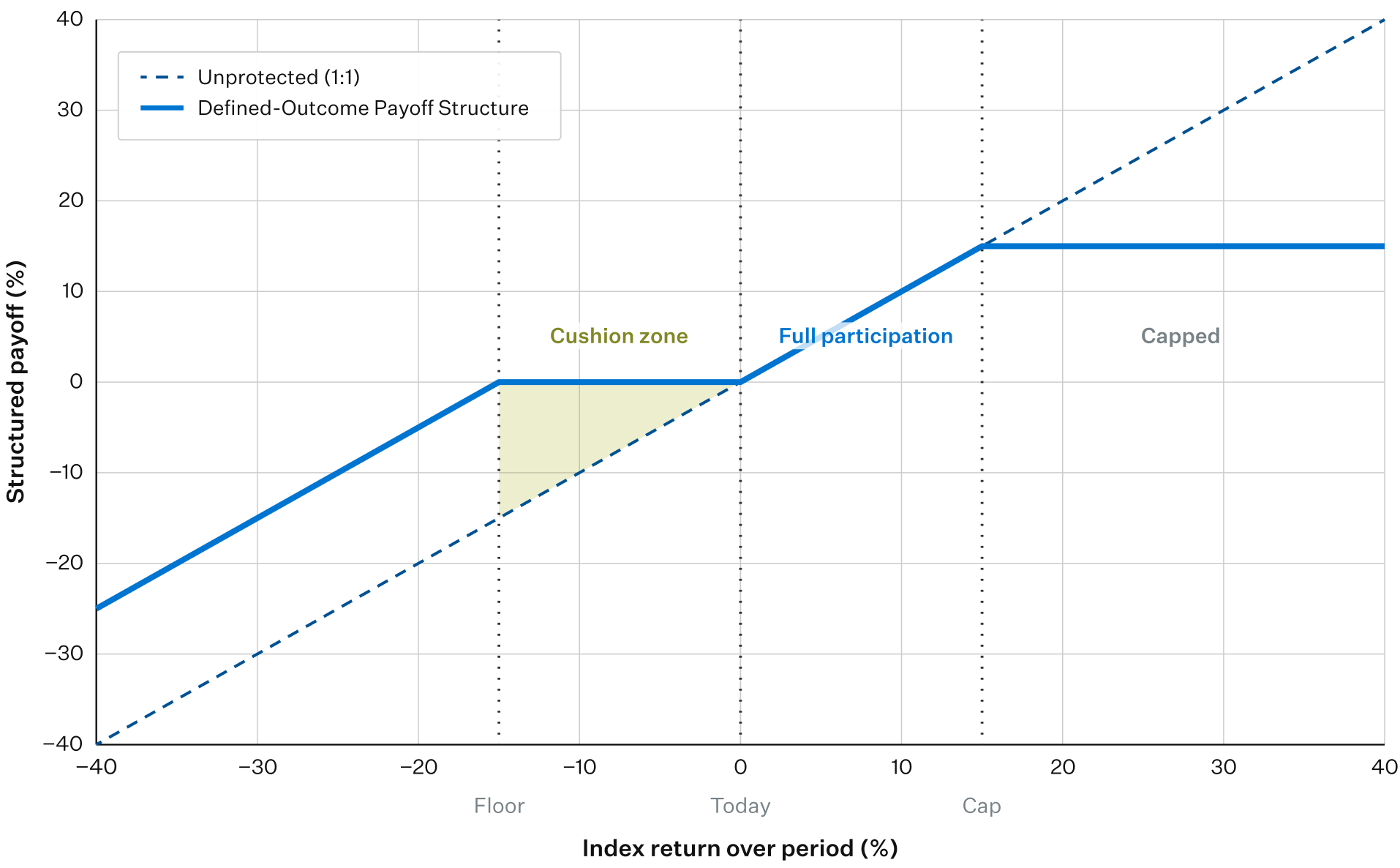

A Concrete Example

Consider a defined-outcome structure with a 15% upside cap and 15% downside cushion over a one-year period. The outcomes across different market scenarios over the one year illustrate how the payoff structure works.

Chart 2. Illustrative payoff profile: Defined-Outcome Payoff Structure (blue) vs. unprotected portfolio (dashed). The shaded zone represents the cushion.

Upside Scenarios

Index up 10%: Return up 10%. Full participation.

Index up 15%: Return up 15%. Full participation at the cap.

Index up 20%: Return up 15%. Participation above the cap is foregone in exchange for downside protection below.

Downside Scenarios

Index down 10%: Return flat. The cushion absorbs the full decline.

Index down 15%: Return flat. Still fully protected within the cushion.

Index down 20%: Return down approximately 5%. The portion of the decline beyond the cushion is absorbed (5% rather than 20%).

For illustrative purposes only. This material is intended to provide only general educational information and is not intended as a solicitation to buy or sell any securities or other financial instruments or to provide any investment advice or service.

The asymmetry here is meaningful. In the most favorable environment—moderate positive returns between 0% and 15%—you keep everything the market delivers. In a material downturn, the cushion significantly limits your overall portfolio loss relative to what an unprotected portfolio would experience. The trade-off is giving up participation above the cap: a scenario most investors are well-positioned to accept, particularly those who are drawing from their portfolios or have a lower tolerance for large interim losses.

Importantly, the structure is designed to be largely self-financing. The premium income collected from selling the upside cap and limiting the downside protection, plus the expected dividends from the ETF over the trade term, offsets the cost of building the protection. Upside participation is balanced against the desired level of downside protection to create a minimal out-of-pocket implementation cost.

How Cap & Cushion Compares to Structured Notes

The conceptual similarity between Cap & Cushion and structured notes is real. Both seek to provide equity participation with downside protection. But the structural differences are material.

Cap & Cushion

Structured notes

Cost

Largely self-financing; no additional management or setup fee beyond custodial transaction costs and Lido's standard advisory fee

Embedded fees paid to the issuing bank reduce the return or starting parameters for the investor

Liquidity

Built from exchange-traded options; positions can generally be adjusted or unwound at current market value

SEC-classified illiquid securities; early exit typically requires a secondary market sale at a discount

Counterparty risk

Options centrally cleared through the OCC; no single-institution exposure

Backed by the issuing bank; investor becomes a general creditor if the institution fails

Customization

Cap level, cushion depth, index, and term set per client; actively managed throughout the contract period

Pre-packaged with fixed terms; limited ability to adjust prior to maturity or an issuer-defined call

Table 3. Cap & Cushion vs. structured notes across four key dimensions.

Counterparty Cost

Investors in structured notes must pay a cost to the third party that creates the structure, typically a bank. This cost can reduce the ultimate return to the investor, as that fee impacts the trade return or initial setup parameters. A Cap & Cushion strategy is deployed directly in client accounts with no additional management or setup fee beyond custodial transaction fees and

Liquidity

Structured notes are classified by the SEC as illiquid securities. Exiting early typically requires selling in a secondary market at a discount or waiting until maturity. Cap & Cushion is constructed using exchange-traded options with deep, liquid markets that trade daily. A client who needs to exit can do so at the current market value of the securities. The liquid nature of the strategy allows your advisor to rebalance or adjust as needed or to be more opportunistic.

Counterparty Risk

A structured note is backed by the issuing bank. Although it’s improbable, it’s conceivable that the bank could fail, in which case, the investor becomes a general creditor. Cap & Cushion holders own publicly traded, generally marketable securities. The options are centrally cleared through the Options Clearing Corp, which acts as a counterparty to all U.S.-listed equity option trades.

Customization and Active Management

Structured notes are pre-packaged products with fixed terms. Cap & Cushion parameters—the cap level, cushion depth, tracked index, and contract period—are set based on each client’s specific objectives and current market conditions. Positions can be actively managed throughout the contract period rather than left static until maturity or a call feature defined by the issuer.

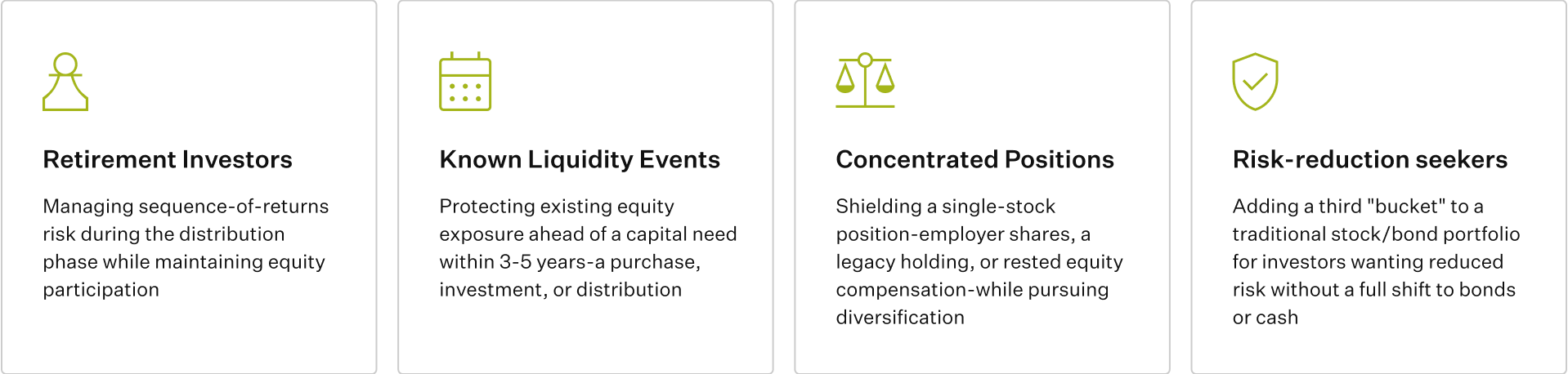

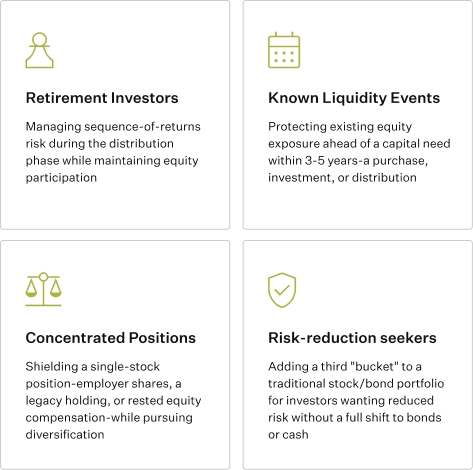

When Cap & Cushion May Be Appropriate

Cap & Cushion is not a strategy for every portfolio or every objective. It is most valuable in specific circumstances where defined outcomes and downside protection have genuine planning utility.

Illustration 4. Four investor profiles for whom Cap & Cushion may offer the most planning utility.

Investors Approaching or in Retirement

Sequence-of-returns risk—the danger that a significant portfolio decline early in retirement forces asset liquidation at depressed prices—is one of the most consequential financial risks for retirees. A large drawdown in the first few years of a distribution phase can permanently impair a portfolio’s ability to support a desired spending level. This is also the first few years of potentially decades of distributions, so some long-term portfolio growth is still a necessity. Cap & Cushion provides a layer of defense, while allowing continued equity participation up to the cap, supporting long-term purchasing power. However, it’s advisable not to draw down funds committed to the Cap & Cushion strategy during the contract period, as doing so may affect the strategy’s effectiveness.

Investors with Known Liquidity Events

For investors who anticipate a capital need from their overall portfolio within 3-5 years, whether for a home purchase, a business investment, a tax payment, or a planned distribution, protecting a specific dollar amount in the existing stock portion of the portfolio over a defined period may be more important than maximizing returns. Cap & Cushion’s defined protection structure maps well onto this kind of time-bound objective for existing stock exposure to accompany traditional cash alternatives or shorter-term debt instruments, such as bonds.

Concentrated Position Holders

For clients managing a significant equity concentration, such as shares held in a single employer stock, a large legacy position, or recently vested equity compensation, Cap & Cushion can help offset portfolio losses in that position in exchange for capping upside. The result is continued upside participation with meaningful protection against concentration risk as you work towards long-term diversification.

A Complementary Risk-Reduction Tool

For investors who would like additional tools to reduce risk but don’t yet need to make a full transition to bonds or cash, Cap & Cushion offers a third bucket for the traditional stock/bond portfolio allocation.

How Lido Implements Cap & Cushion

At Lido Advisors, Cap & Cushion is implemented as part of a coordinated wealth management strategy, not as a standalone product. Before recommending any variation of the strategy, we evaluate the client’s full financial picture, including income needs, tax situation, existing equity exposures, liquidity requirements, time horizon, and risk tolerance.

The strategy is built and managed by Lido’s investment team, the same professionals who oversee broader portfolio construction, alternative investments, and equity compensation planning. Parameters are set based on current market conditions and the client’s specific objectives, and positions are actively monitored and adjusted as conditions change.

Because the strategy is constructed inside the client’s own account using exchange-traded instruments, all positions in the strategy are visible at all times. There are no black-box mechanics, no embedded fees that require reverse-engineering to understand, and no external manager relationships to coordinate.

Jeff Garden, Lido’s Chief Investment Officer, frames the philosophy this way: “The more complex the portfolio, the greater the need to manage the outcome with tools such as alternatives, options, and defined outcome strategies.” Cap & Cushion is one way Lido answers that need. It’s a purpose-built tool for managing individual and consequential risk.

Frequently Asked Questions

How is Cap & Cushion different from a structured note?

The conceptual goal of Cap & Cushion is similar to that of a structured note. Both can provide equity participation with downside protection, but the execution differs in ways that matter. Cap & Cushion is built from exchange-traded options inside the client’s own account, with no additional third-party costs. Unlike bank-issued structured notes, there is no issuer counterparty risk; options are centrally cleared through the Options Clearing Corporation.

Is the downside protection guaranteed?

Cap & Cushion is designed to provide protection within a defined range and over a defined period. It is not an insurance product, and outcomes can differ from the design if positions are exited early or if market conditions produce returns outside the protection range. There is no guarantee that the strategy will avoid losses. Lido actively manages positions to pursue the stated objectives, but all investing involves risk.

What index does Cap & Cushion track?

The strategy most commonly tracks the S&P 500, but the underlying index or stock, cap level, cushion depth, and contract period can be customized to each client’s objectives and current market conditions. Parameters vary across clients and can be adjusted over time.

Does Cap & Cushion work for concentrated stock positions?

Yes, with adaptations if there is a liquid options market around the concentrated position or a close proxy, and the investor is not prevented from hedging via options or selling the position for any reason.

How liquid is Cap & Cushion?

The strategy is constructed from exchange-traded options that trade in liquid markets daily. Unlike structured notes, which may require a secondary market transaction at a discount to exit early, Cap & Cushion positions can generally be adjusted or unwound at the then-current market price. That said, any stated defined outcome is based on holding to the expiration, and early adjustments may affect realized outcomes.

What does Cap & Cushion cost?

Because the strategy is designed to be largely self-financing, with premiums collected from selling the upside cap and elements of the downside structure to offset costs, there is typically no significant out-of-pocket cost to implement. The tradeoff is capping upside participation at the agreed level. Lido’s in-house capabilities allow the strategy to be executed without external manager fees or product markups. This strategy is still subject to a client’s general Lido management fee.

Ready to Explore Cap & Cushion?

Managing downside risk without sacrificing long-term growth potential is one of the central challenges of wealth management. Cap & Cushion offers a transparent, liquid, and cost-efficient alternative to conventional defensive strategies, built on the same mechanics as bank-issued structured products but constructed directly in your account and actively managed on your behalf.

Lido Advisors works with clients across a range of equity exposures and planning objectives to determine when and how Cap & Cushion fits within a broader investment strategy.

Disclaimer

Lido Advisors, LLC is an SEC-registered investment adviser. Please note that SEC registration does not denote any particular competence or ability, and no inference to the contrary should be made. For complete information on the services we provide and our fees, please review our Form ADV at adviserinfo.sec.gov, call (310) 278-8232, or mail us at 1875 Century Park East, Suite 950, Los Angeles, CA 90067.

Past performance is not indicative of future performance. The information in this report is for informational purposes only and should not be relied upon as the basis of an investment or liquidation decision. Nothing in this report shall be construed to be a solicitation to buy or offer to sell any security, product, or service to any non-U.S. investor, nor shall any such security, product or service be solicited, offered or sold in any jurisdiction where such activity would be contrary to the securities laws or other local laws and regulations or would subject Lido to any registration requirement within such jurisdiction. Certain information contained in these materials has been obtained from published and unpublished sources prepared by third parties, which, in certain cases, have not been updated through the date hereof. While such information is believed to be reliable, Lido has not independently verified such information, nor does it assume any responsibility for the accuracy or completeness of such information. Except as otherwise indicated herein, the information, opinions, and estimates provided in this presentation are based on matters and information as they exist as of the date these materials have been prepared and not as of any future date, and will not be updated or otherwise revised to reflect information that is subsequently discovered or available, or for changes in circumstances occurring after the date hereof. Lido’s opinions and estimates constitute Lido’s judgment and should be regarded as indicative, preliminary, and for illustrative purposes only.

Not all investments are suitable for all clients. It should not be assumed that any security listed or any recommendations made in the future will be profitable or without loss, including risk of loss of principal, or will equal any prior performance. All investments involve the risk of potential investment losses, including the potential risk of loss of principal, as well as the potential for investment gain. Further, the prior yield figures indicated herein represent performance for only a short time period and may not be indicative of the yield or volatility each security will generate over a long time period. The yield should also be viewed in the context of the broad market and general economic conditions prevailing during the periods covered by the performance information. Any references to future returns/risk are not promises of the actual return the client portfolio may achieve. Before investing, investors should seek financial advice regarding the appropriateness of investing in any securities or investment strategies discussed. Not all investments are suitable for all investors.

Certain information contained in this document constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “seek,” “expect,” “anticipate,” “target,” “project,” “estimate,” “intend,” “continue,” “believe,” the negatives thereof, other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events or results or the actual performance of the Fund may differ materially from those reflected or contemplated in such forward-looking statements.