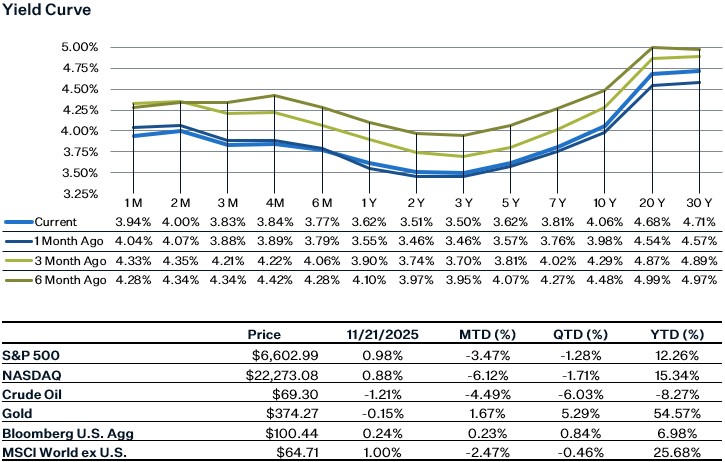

Market Update

U.S. equity markets had a highly volatile week last week, as investors had knee-jerk responses from the incoming data and Fed commentary and their impact on rate cut expectations for December. Additionally, despite NVDA beating on Q3 earnings and raising revenue guidance for Q4, investors seem to remain cautious around AI valuations. The October FOMC minutes released on Wednesday showed an ongoing divide between members regarding the appropriate monetary policy decision for December. The jobs report for September showed that job gains were higher than anticipated, but there was weakness in other metrics. Payroll growth was revised downward by 26K to –4k in August and by 7k to 72k in July, however the market’s initial reaction was that the jobs report was decent enough for the Fed to possibly keep rates on hold in December. However, due to NY Fed President Williams’ dovish comments on Friday morning, the rate probabilities essentially reversed and went back up to 70% by the end of the day. This week is typically a relatively muted week for the markets given the holiday but expect investors to be highly focused on any incoming economic data that we get ahead of the Fed’s meeting on December 10th.

September Jobs Report

The headline number for the September jobs report came in better than expected, up 119k versus consensus expectations of a 50k increase. Job gains were concentrated in healthcare and social assistance (+57k) and leisure and hospitality industries (+47K). Retail trade job gains were 14k for the month, which is in line with September’s number from last year, which could suggest that the consumer is still doing ok. Construction jobs increased 19k, while transportation and warehousing jobs declined by 25k for the month. The unemployment rate ticked up to 4.4% from 4.3%, but this was partly due to an increase in labor force participation – from 62.3% to 62.4%. There were weak areas in the report, however. Wage growth was lower than expected, and revisions for both July and August were revised down. Average hourly earnings rose 0.2% month-over-month, lower than the expected 0.3% increase although annualized remains steady at 3.8%. Additionally, permanent job losers rose to over 2 million, the highest level reached since October 2021.

Given the government shutdown, this data is pretty stale and might not be that indicative of the current labor situation. The BLS will not release household survey data for October, meaning we won’t get an unemployment number for that month. Additionally, the establishment survey data for October is scheduled to be released on December 16th with the November report, so there likely won't be much emphasis placed on October as the November data will be timelier. More importantly, the delayed release of the November jobs report means that the Federal Reserve will not have updated jobs data from the BLS before their December meeting. This makes the Fed’s job particularly difficult this time around, as they are carefully balancing the conflicting risks of sticky inflation and a weak labor market going into their meeting.

US Trade Deficit Narrows

The US trade deficit for August 2025 came in narrower than expected, at $59.6 billion, versus economists' expectations of $60.4 billion. The narrower deficit was driven primarily by a 5.1% month-over-month drop in imports, including a notable decline in nonmonetary gold imports linked to Swiss tariffs. However, since the US and Switzerland have since reached a trade deal to lower these tariffs, this drop is likely a short-term development rather than a sustained trend. Meanwhile, exports inched up 0.1% month-over-month, driven entirely by services such as travel and repair, while goods exports declined, weighed down by softer consumer products and pharmaceutical shipments. US GDP is expected to get a tailwind from lighter trade deficits, as narrower deficits play into stronger GDP through the net exports channel. President Trump's tariffs seem to be affecting trade flows by reducing aggregate imports; however, in the future, developments such as trade deals with other countries and the Supreme Court's ruling on the constitutionality of tariffs may play a significant role in shaping trade flows.

November US Manufacturing PMI

The US manufacturing PMI slipped from 52.5 in October to 51.9 in November, slightly below the 52.0 figure economists had expected. The culprits behind the weaker-than-expected number were slower new orders, high inventory levels, and higher prices due to tariffs. A crucial metric to watch is how the unsold goods figures continue to develop, as inventory accumulation may indicate that factory expansion is slowing and thereby potentially spilling over into the service sector. Although the manufacturing sector may no longer be as crucial to the US economy as it once was, it still accounts for around 10.2% of the economy and may offer an insight into how the administration's protectionist policies have been affecting a sector they aim to revive. Thus far, however, manufacturers have been feeling the brunt of the tariffs, with many stating that high input costs have been a drag, and lower- and middle-income consumers’ economic uncertainty has reduced demand.

Sources:

https://markets.jpmorgan.com/jpmm/research.article_page?action=open&doc=GPS-5140051-0

https://www.bls.gov/news.release/pdf/empsit.pd

https://fred.stlouisfed.org/series/LNS13026638

https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

https://www.reuters.com/business/us-trade-deficit-narrows-sharply-august-imports-fall-2025-11-19/