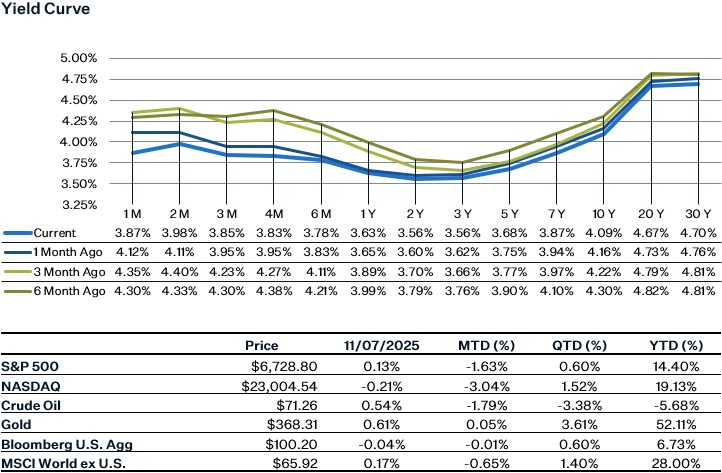

Market Update

U.S. equity markets ended the week down last week, as AI worries surfaced and economic reports gave mixed messages on the economy. AI circularity issues and valuation concerns were one of the main drivers for the pullback last week, with many companies fueling each other’s AI capex spend commitments. Additionally, despite a strong Q3 earnings season, investors remain cautious as the market has been rewarding earnings beats less than average. Brief optimism was ignited on Friday as the Democrats proposed a plan to end the government shutdown, however Republicans quickly rejected the deal. On the economic data front we received mixed messages about the state of the labor market, with the ADP payrolls report showing a rebound in job gains for October while the Challenger survey showed a surge of layoffs. Until the release of federal economic data resumes, investors are likely to remain cautious and sit on the sidelines until there is more clarity on the economy.

Labor Market Rollercoaster

Last week we got some data on the labor market, however the data appear to be at odds with each other, telling two different stories. The ADP payrolls report gave us a sanguine picture of the labor market, with the October report showing that private payrolls increased by 42k for the month, a sharp reversal from the 29k decline that was reported in September.

On the other hand, the Challenger Report survey results struck an ominous tone, with job cuts surging to over 153k for the month of October which was nearly triple the number of cuts in September. Job cuts year-to-date for the private sector are also the most cuts since COVID in 2020 and before that the most cuts since 2009. Cost-cutting was the top reason cited by employers as the reason for layoffs, followed by AI. Looking at different industries - retailers, warehousing, and non-profits (due to cuts in government funding) have experienced the largest percentage increases in job cuts so far this year. However, looking more into the details, over half of the layoffs for October came from two states – Georgia and Washington. If you exclude those layoffs, the increase in job cuts is not as stark compared to the same period last year but there is still a notable increase.

September Services PMI

The services PMI for September registered at 50.0, marking the first time the index has reached this level since 2010. Concerning trends appeared in the Business Activity index, which decreased from 55.0 last month to 49.9, marking the first time since May 2020 that the index has officially entered a contraction. Reasons for the decrease were noted as slower overall demand, with particular industries - such as mining, construction, and real estate, being particularly affected. The New Order index reflected similar concerns, with the index now barely expanding, as factors such as supply chain issues and economic uncertainty continued to drag it down. The employment index improved month over month, yet it remains in contractionary territory for the fourth consecutive month, as AI efficiencies and persistent hiring freezes limited job growth. In contrast, the information technology segment has been seeing strong demand for AI and cloud-related products, with order backlogs being slightly elevated for the month but still manageable.

Holiday Spending

The NRF expects Americans to spend between $1.01 trillion and $1.02 trillion for the first time, representing an increase between 3.7% to 4.2% above last year's spending. Healthy holiday spending is crucial for retailers, as holiday sales can often account for 19% of annual retail sales, and consumer spending as a whole comprises 70% of the U.S. GDP. Thus far, although holiday spending growth has moderated from the past couple of years, it still remains higher than the pre-COVID average of 3.6% year-over-year growth. The main driver of the increase in holiday spending has stemmed from higher-income households, as these consumers have been able to absorb price increases from tariffs and have enjoyed higher wage gains than their lower-income peers. Meanwhile, lower-income households have been constrained by tepid wage gains and higher prices, causing many of them to rely on credit cards and engage in bargain hunting for holiday shopping.

Sources:

https://www.challengergray.com/blog/october-challenger-report-153074-job-cuts-on-cost-cutting-ai/

https://www.challengergray.com/wp-content/uploads/2025/11/Challenger-Report-October-2025.pdf

https://adpemploymentreport.com/