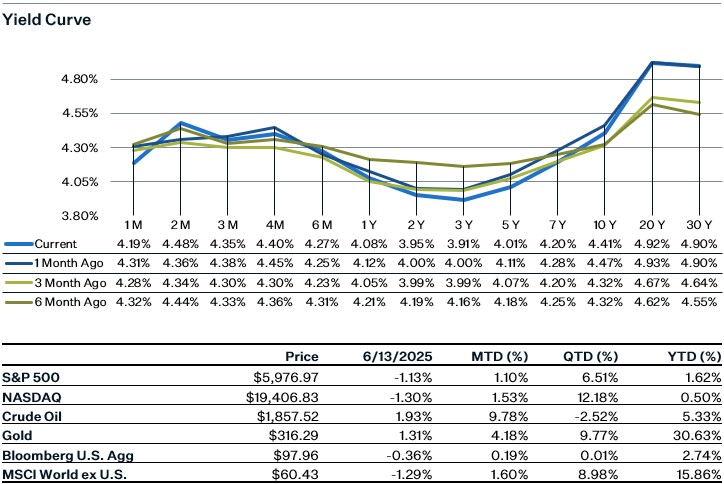

Market Update

Positive inflation data boosted sentiment and lifted markets earlier in the week, but Friday's worrying news of rising tensions in the Middle East pushed oil prices higher and reintroduced a fresh wave of uncertainty to an already volatile backdrop, ultimately causing the S&P to end lower for the week. The spike in oil was the main area of concern, as it could increase inflation concerns and weigh on the global economy. Separately, we got some positive news on the China-US trade deal, with China reported to supply critical rare minerals to the U.S. while the U.S. would allow Chinese students to attend U.S. universities. The agreement has yet to be finalized though, so there’s still the risk that either party could tarnish the deal. This week we have retail sales data on Tuesday and the June FOMC meeting on Wednesday, when we’ll get an updated Summary of Economic Projections from the Federal Reserve.

Consumer Price Index

Inflation data for May surprised by coming lower than expected, with both headline and core CPI rising just 0.1% month over month. Headline CPI is now at 2.4% year-over-year (YoY), while core CPI remains steady at 2.8% YoY. The softness was largely driven by a 1% decline in energy prices and continued weakness in vehicle prices. Shelter inflation showed further deceleration, with rents and owners’ equivalent rent rising more moderately (0.27%), and the supercore index, excluding shelter, rising just 0.06%. On a three-month annualized basis, rent shelter is running around 3.6%, still above pre-pandemic trend while supercore has slowed to near zero at 0.1%, suggesting service-sector price stickiness is fading.

As for tariffs, their broad inflationary impact has been limited so far. While toys and major appliances recorded notable price increases, categories like apparel and vehicles declined, indicating many firms are either absorbing higher costs or drawing from pre-tariff inventories. However, according to recent regional Fed surveys, at least half of tariff-affected firms plan to pass on costs within the next three months, potentially pushing more visible price effects into late summer.

Producer Price Index

The May headline producer price index (PPI) rose 0.1% month-over-month, below expectations. Both food and energy prices were little changed in May, with food up 0.1% and energy flat for the month. Core PPI rose 0.1% for the month as well. Some categories that are susceptible to tariffs have seen notable increases such as metal manufacturing, metal products, electrical equipment, and household appliances. However, others, such as machinery and transportation equipment, have not seen significant jumps yet. Overall, the PPI and CPI numbers for May were relatively benign and likely only reflect the early stages of the tariff impact on inflation.

Consumer Sentiment

The preliminary University of Michigan Consumer Sentiment Index rose by more than 8 points to 60.5, fueled by optimism following the China trade deal and a rebound in equity markets. This is the first survey to fully reflect post-deal sentiment. Most of the improvement came from a 10.5-point jump in future expectations, while current conditions rose by 5 points. Despite the uptick, the report notes that consumers still perceive broad downside risks to the economy. Inflation expectations also eased, with the one-year outlook falling to 5.1% from 6.6%, and long-term expectations edging down slightly from 4.2% to 4.1%.

Sources:

https://www.bls.gov/news.release/archives/ppi_06122025.htm

https://www.sca.isr.umich.edu/