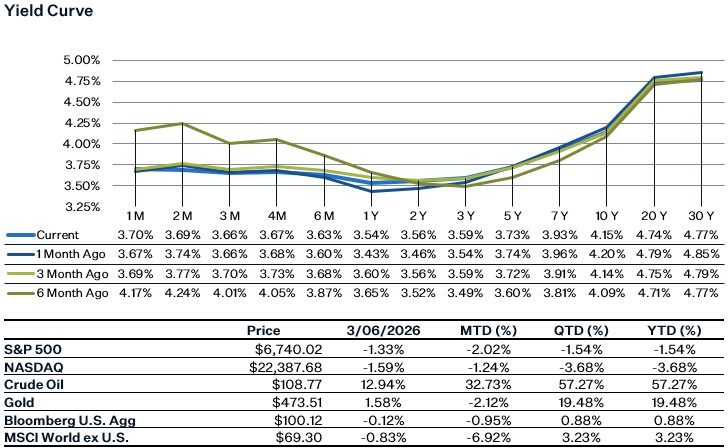

Market Update

Geopolitical tensions and the rising uncertainty around the Iran conflict dominated sentiment last week, with all major U.S. equity indices registering a notable pullback. The main concern regarding the conflict is unsurprisingly the impact it will have on oil and energy flows/prices, and the repercussions this has on inflation and economic growth. Given the world’s heavy dependence on oil and the inflation risks associated with supply disruptions, the S&P 500 declined 1.24% last week. International markets were more heavily affected, with the MSCI ACWI ex-U.S. falling 4.56% for the week. International indices were hit harder given their greater reliance on imported energy. On the economic front, the Federal Reserve received a mixed employment report on Friday. The jobs report for February came in below estimates, showing a decline in jobs of 92k. However, the establishment survey's payroll prints remain subject to material revision risk despite BLS modifying the model to incorporate real time sample data. The household survey, while noisier month-to-month, doesn't embed the same model-driven risk and depicts a labor market that is softening but not deteriorating in a disorderly way.

February Jobs Report

The February jobs report came in weaker than expected, with employment falling for the month versus an anticipated increase. Nonfarm payrolls for February fell by 92k, a sharp contrast to the consensus estimate of a gain of 60k. Additionally, payrolls for January and December were revised down. Most industries recorded job losses in February; however the losses were particularly concentrated in the leisure and hospitality, healthcare, and educational services industries. One of the reasons for the fall in healthcare jobs was due to a strike from healthcare workers. Given that the strike has ended, we will likely see a rebound in healthcare employment in March.

Looking at other details in the report, the unemployment rate ticked up to 4.4%, compared to expectations of remaining at 4.3%. A tick up in unemployment isn’t usually a big deal, but over the past year it has been slowly creeping up and a continued increase in unemployment from here would be a sign that labor demand is worryingly weak. Average hourly earnings came in stronger than expected at 0.4% for the month, but it looks like a lot of the strength is coming from goods-producing industries, with larger than average increases for construction and manufacturing workers. Although this report was weak overall, market expectations for Fed rate cuts haven’t changed. It will likely take a series of weak job reports before investors move up their rate cut forecasts.

International Markets Roil from the Closure at the Strait of Hormuz

Asian equities broadly declined amid the ongoing US-Iran conflict, as the closure of the Strait of Hormuz pushed oil prices higher and disrupted the delivery of liquified natural gas (LNG) to importers. Tech and industrial Asian nations such as South Korea and Japan are particularly exposed to the ongoing disruptions, with both countries sourcing over 70% of their energy imports from the Middle East. To make matters worse, both nations have virtually no domestic capacity to meet their energy needs, meaning governments on both sides have started to loosen the grip on their crude and LNG strategic reserves to maintain a steady energy supply. In contrast, China, although it purchases over 90% of Iran’s oil exports, has not experienced the same level of market volatility as other countries, largely because its domestic energy production, diversified supply routes, and large strategic petroleum reserves provide it with a much larger energy buffer than its neighbors. The downstream effects of persistently higher energy prices are likely to put pressure on margins for energy intensive industrials, increase the likelihood of short-term inflationary pressures, and create uncertainty about how each country’s central bank will respond. Moving ahead, if the war concludes quickly and shipping companies determine that travel through the Strait is safe again, cost pressures could subside quickly as business operations return to normal. However, if uncertainty continues to linger in the region, Asian equities are likely to remain volatile as growth assumptions are questioned, risk premiums rise, and currencies weaken in countries struggling with resurgent inflation.

Sources:

https://markets.jpmorgan.com/jpmm/research.article_page?action=open&doc=GPS-5221696-0

https://markets.jpmorgan.com/jpmm/research.article_page?action=open&doc=GPS-5227927-0

https://www.cnbc.com/2026/03/03/strait-of-hormuz-closure-which-countries-will-be-hit-the-most.html

https://www.bls.gov/news.release/pdf/empsit.pdf