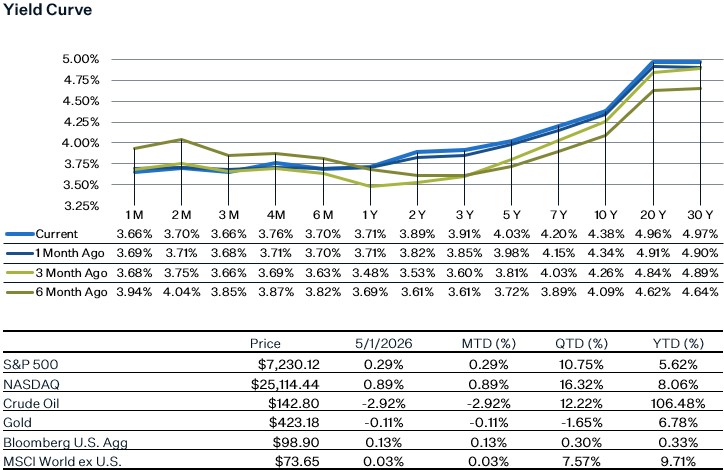

Market Update – April Recap

April marked a complete reversal in investor sentiment leading to record rallies across most indices, with the S&P 500 ending the month up nearly 10.5%, its best month since November 2020. The US-Iran ceasefire was the main tailwind in the beginning of the month, as the market focused on de-escalation despite the Strait of Hormuz remaining effectively off limits and causing continued energy supply disruption. The war with Iran continues to offer a lot of headline noise, but ultimately the timeline for a resolution remains unclear as negotiations have stalled. Given the inflation risks, the market is now pricing in zero Fed rate cuts this year. Looking at the yield curve, rates rose slightly across almost every part of the curve, with the 10-year treasury yield reaching 4.4% at the end of the month.

Besides the ceasefire, earnings upgrades were a key driver of the strong returns for the month. Technology and AI-related stocks led the market higher in April as the AI optimism narrative returned in full force. The Mag 7 stocks all ended the month higher with GOOGL (+33.9%) and AMZN (+27.3%) the two big outperformers. Additionally, the market rewarded AI capex receivers such as semi and memory stocks, with the semiconductor ETF SOXX having its second-best month on record, up over 40%. Q1 earnings results are coming in very strong so far, with 84% of companies that have reported beating estimates, above the 5-year average of 78%. The Mag 7 earnings showed yet another increase in capex spending forecasts - the hyperscalers increased their 2026 capex forecasts by $100B to over $700B. Diving a bit into the details of the reports, GOOGL delivered record 63% revenue growth in its Cloud segment due to strong AI demand, while AMZN recorded a fifth straight quarter of growing AWS revenue. Meanwhile, investors were disappointed with META’s weaker-than-expected revenue guidance alongside a higher capex outlook. On top of more earnings this week, we have the BLS jobs report for April coming out on Friday. Consensus expectations are for the economy to add 68k jobs and for the unemployment rate to remain steady at 4.3%.

April FOMC Meeting

As expected, the Federal Reserve let policy rates unchanged last week, with the fed funds rate remaining at 3.5 – 3.75%. The main reason behind keeping rates on hold was due to higher inflation, with the post-meeting statement stating that “Inflation is elevated, in part reflecting the recent increase in global energy prices.” The more interesting takeaways from the meeting however were that 3 voting members voted against maintaining an easing bias in the statement and news from Chair Powell stating that he will remain on the committee for some time as a Governor once his chairmanship term is up. In regard to the 3 members’ dissents, the dissent was referring to a sentence in the statement that says, “In considering the extent and timing of additional adjustments to the target…”. While the statement doesn’t explicitly mention rate cuts, the wording has been in place since the last cut—so “additional adjustments” could reasonably be interpreted as signaling further cuts. What matters is that the dissents suggest there is a growing group of members who view rate hikes just as likely as cuts for the next policy move. Given the ongoing war’s impact on inflation expectations and the slight hawkishness from certain Fed members, the market is currently not pricing in any rate cuts for 2026 and has pushed out rate cuts for 2027 until late in the year.

Q1 GDP & March PCE

Real GDP growth for Q1 2026 came in at 2.0%, a slight miss versus the 2.3% consensus. The primary drivers of Real GDP growth were consumer spending, supported in part by higher tax refunds, and business investment, which grew 10.4%, the fastest pace in nearly three years, driven largely by AI-related spending on equipment and software. On the negative side, net exports subtracted 1.3 percentage points from GDP, the most in over a year, reflecting a surge in tech-related imports, and meanwhile, government spending rebounded after being depressed by the federal shutdown in Q4. Released alongside the GDP report, the Fed’s preferred inflation gauge, core PCE, also came out, printing a figure of 3.2%, in line with market expectations, but it was also the highest since November 2023. Unsurprisingly, energy shocks were the main reason for the jump in the PCE, as oil is up 56% and gasoline is up 44% since the start of the conflict. The jump in energy prices is likely to continue bleeding into the economy by raising input costs across a wide swath of industries, and it has the secondary effect of reducing discretionary consumption, as every dollar spent on higher energy prices is taken from other areas. Overall, the mix of the two reports paints a picture of an economy that is continuing to grow, yet the largest component of the GDP, the consumer, remains under stress due to the continued presence of higher prices, and the continued strength in business investments due to AI might be simultaneously concealing some of that underlying weakness in the consumer.

Sources:

https://www.bea.gov/news/2026/gdp-advance-estimate-1st-quarter-2026

https://www.bea.gov/news/2026/personal-income-and-outlays-march-2026

https://www.federalreserve.gov/monetarypolicy/files/monetary20260429a1.pdf

https://www.federalreserve.gov/mediacenter/files/FOMCpresconf20260429.pdf