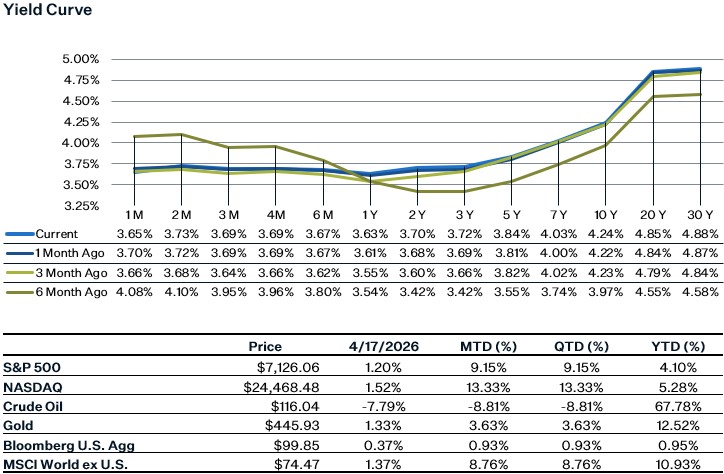

Market Update

Investor optimism was back in full force last week, with all the major U.S. indices experiencing a strong rally on the backs of hopes for a near-term resolution with Iran following positive news regarding the Strait of Hormuz. Throughout the week there were notes of positive discussions between the US and Iran, and on Friday Iran's Foreign Minister stated that passage for all commercial vessels through the Strait of Hormuz is “completely open” for the remainder of the ceasefire. Given the potential tailwinds to the economy and companies, stocks posted strong gains, with the S&P 500 reaching its first record close since late January. The U.S. continues to maintain its blockade in the Strait however, and events over the weekend have cast doubts on a quick resolution. Given the most recent events, it’s likely that negotiation talks will drag on for some time, which means continued economic uncertainty. As such, we expect market volatility to continue in the near term. In terms of economic data, this week we have March retail sales data on Tuesday which will be closely watched by investors to see if there are any signs of consumer weakness amidst higher energy prices. Additionally, Kevin Warsh’s nomination hearing for Fed Chair is also scheduled for Tuesday. Earnings reports ramp up this week as well, with approximately 19% of S&P 500 companies reporting throughout the week. The estimated earnings growth rate for the S&P 500 is a healthy 12.6% for Q1. Main topics of discussion during the earnings calls will likely be: 1) AI disruption concerns, 2) impact of higher input costs on corporate margins, and 3) any change in consumer spending habits since the war and consumer outlook going forward.

March PPI

The March PPI report came in cooler than expected, with the headline number coming in at 0.5% on a month-over-month basis, while expectations were set for a rise of 1.0%. The coolness in the headline number came as a surprise, especially as energy costs jumped 8.5% for the month and diesel prices soared by 42%, but the offset came from a surprising decline in food costs and flatness in total services. Core PPI also continued the surprise to the downside theme, as the figure came in at a 0.1% increase, while expectations were for a print of 0.3%. Interestingly, one of the main reasons for the cool Core PPI print was that wholesalers did not pass on the higher input costs to retailers, as evidenced by a 6.0% decline in food and alcohol wholesaling margins. The suggestions here likely signals that firms either expect energy shocks to be a short-term phenomenon or that tariff pass-through price hikes may be easing. Regardless, it's important to keep in mind that the PPI is still running at 4.0% year over year, the highest reading in over three years, and with some PPI components feeding into the PCE price index, the Federal Reserve might find itself in an uncomfortable spot where it prefers to hold rates rather than cut.

March CPI Report

Headline CPI increased 0.9% for the month of March, bringing the year-over-year rate up to 3.3% from February’s 2.4% rate. The spike in headline inflation was unsurprisingly due to an increase in energy prices from the war, with gasoline prices increasing 21.2% for the month, the largest monthly increase since tracking the metric began in 1967, while fuel oil (related to residential heating oil) prices increased a staggering 30.7% for the month. Food prices were unchanged for the month, although it’s likely that we could see an acceleration in food prices in the coming months as higher fuel and fertilizer costs could force grocery companies to raise prices.

There were some brighter aspects of the report when looking at core. Core inflation increased 0.2% for the month, slightly lower than expectations of 0.3%. However, the year-over-year rate remains elevated and increased, going from 2.5% in February to 2.6% in March. Looking at some of the components in core, used car prices fell while airline fares increased 2.7% for the month, as airlines attempt to mitigate profit erosion by raising ticket prices and fees for other services. Shelter inflation remains stable, increasing 0.3% for the month. Given that inflation numbers were mostly in line with expectations, the Fed will likely remain in wait and see mode until there is more clarity around the path of inflation.

Sources:

https://www.bls.gov/news.release/ppi.nr0.htm?

https://markets.jpmorgan.com/jpmm/research.article_page?action=open&doc=GPS-5267769-0

https://www.bls.gov/news.release/pdf/cpi.pdf