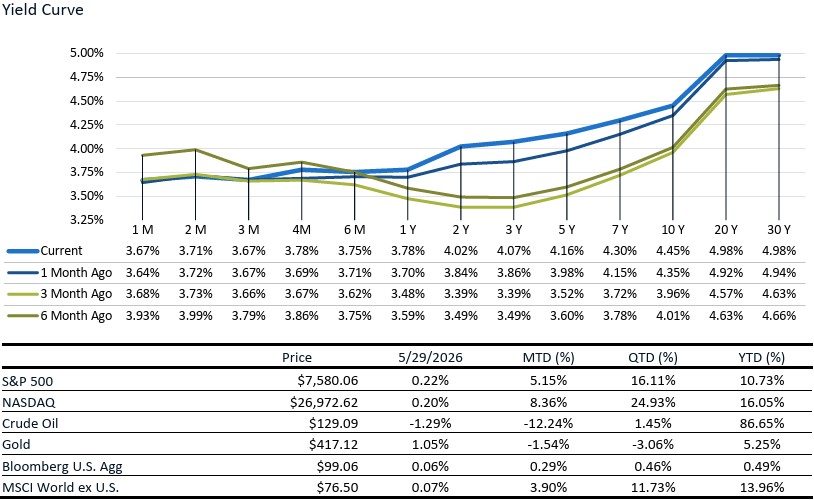

Market Update

Hope for a ceasefire was one of the dominant market themes last week, helping push stocks higher while oil prices and bond yields moved lower, even as questions remain around whether a formal agreement will ultimately be reached. The S&P 500 posted its ninth consecutive weekly gain and is now up 10.7% year-todate, with much of the advance driven by the continued AI demand story. Earnings from AI-related hardware companies continued to come in overwhelmingly strong, most notably Dell’s earnings last week as they reported a 757% year-over-year increase in AI server revenue. Software names also saw a rebound last week, as SNOW’s strong earnings alleviated some concerns around AI disruption for software companies. On the economic front, first-quarter GDP was revised down to a 1.6% annualized pace from the initial 2.0% estimate. However, the underlying data suggests the economy remains more resilient than the headline implies. Business investment, particularly in technology and AI infrastructure, continues to be a key source of strength. At the same time, consumer spending remains positive, though personal income was largely flat in April, suggesting households are increasingly relying on savings and other sources of liquidity to maintain spending. Pressure on household incomes, slowing corporate profit growth, and inflation that remains above the Fed's target are the major economic headwinds as we move through the second half of the year. We have the jobs report for May being released this week on Friday, which will likely show another month of modest job gains and no change to the unemployment rate.

GDP Second Estimate

First-quarter GDP was revised down to 1.6% from the initial 2.0% estimate, primarily due to lower inventory accumulation and softer healthcare spending. However, the underlying picture remains more constructive than the headline suggests. Real final sales to private domestic purchasers, a key measure of underlying demand that exclude inventories and trade, held steady at 2.4%, indicating that consumers and businesses continue to support economic growth. One of the strongest areas of the economy remains business investment, particularly in technology and AI infrastructure, as companies continue spending on data centers, computing equipment, and related projects. Consumer spending also remained positive during the quarter, helping offset some of the softer areas of the report. That said, there are signs the economy is becoming more uneven. Inflation remains elevated, limiting the Fed's flexibility to lower interest rates. In addition, income growth is beginning to lag overall economic activity, while corporate profit growth slowed considerably from the prior quarter. Overall, the economy remains supported by healthy private demand and AI-related capital spending, but elevated inflation combined with slowing income and profit growth are key risks.

PCE and Personal Income

Core PCE inflation rose 0.24% month-over-month, bringing the year-over-year rate up from 3.2% to 3.3%. The latest PCE reading reinforces the notion that the Fed will likely remain on hold for the next several meetings. Real disposable income growth year-over-year is now negative given the recent notable rise in headline inflation. The inflationary headwind to consumer wallets has resulted in savings rates dropping again, falling to 2.6% which is the lowest rate since June 2022. Looking at the change in monthly consumer spending, we can see that the consumer increased their spending most in essential categories such as gasoline and housing and utilities. On the other hand, consumer spending decreased month-over-month for clothing and footwear and motor vehicles and parts categories. Investors will likely be watching consumer spending closely to see if this trend of reducing discretionary spending to fund essentials strengthens in the coming months.

Earnings – An Update to the AI Narrative

Last week, a slew of companies across different layers of the tech stack all reported earnings, providing the market with a clear read as to how each layer is being impacted by the AI buildout. SNPS, a foundational EDA provider, stated that AI demand is increasing the volume and complexity of chips, creating tailwinds for its EDA and simulation portfolio. Of interest was the firm saying it plans to reprice hyperscaler contracts at the end of FY 26, since it recognizes that its tools have pivoted from being used solely by engineers to a mix of engineers and agents consuming its products; all of which is setting up the company to reshape its product monetization from seat-based to one that is more consumption-based for both humans and agents. On the silicon layer, MRVL confirmed the ongoing diversification of hyperscalers from buying NVDA GPUs solely to now building their own ASICs, all in an effort to make the economics of data centers more favorable. ASIC demand from both MSFT and AMZN has propelled massive growth in MRVL’s data center solutions, with the segment now accounting for 76% of total revenue, up from just 40% in 2024, and with contracts now being worked out, it only increases revenue visibility going forward. Lastly, on the software side, results were mixed - SNOW impressed investors with its Cortex Code (CoCo), showing that CoCo is making it easier to shift workloads from legacy data platforms to more modern ones and is driving increased internal sales productivity. Meanwhile, for applications like CRM, although results with Agentforce continue to show increased spending among customers who use the product, the market instead focused on softer-than-expected sales guidance and backlog results meeting market expectations. Taken as a whole, the news demonstrates that AI monetization remains prevalent in both the silicon and data infrastructure layer, but other areas, such as the applications and even design layer, have yet to fully figure out how to monetize the technology.

Sources:

https://www.bea.gov/news/2026/gdp-second-estimate-and-corporate-profits-1st-quarter-2026 https://marquee.gs.com/content/research/en/reports/2026/05/29/bbc3dd73-d969-43bd-8521-f2bd1735ecb9.html https://markets.jpmorgan.com/jpmm/research.article_page?action=open&doc=GPS-5320231-0 https://marquee.gs.com/content/research/en/reports/2026/05/28/4ff758a0-6db3-4fcd-88cb-d891d53d83bc.html https://marquee.gs.com/content/research/en/reports/2026/05/28/108d16dc-cabd-43c9-8a9b-e6649ddd8c59.html https://marquee.gs.com/content/research/en/reports/2026/05/28/3e068035-e3e5-483c-8f33-3e64a3f43d85.html https://marquee.gs.com/content/research/en/reports/2026/05/28/f3415d37-68c2-4c5a-b4fe-c27fc755035d.html https://www.bea.gov/data/personal-consumption-expenditures-price-index-excluding-food-and-energy https://www.cnbc.com/2026/05/29/dell-stock-earnings-ai-servers.html