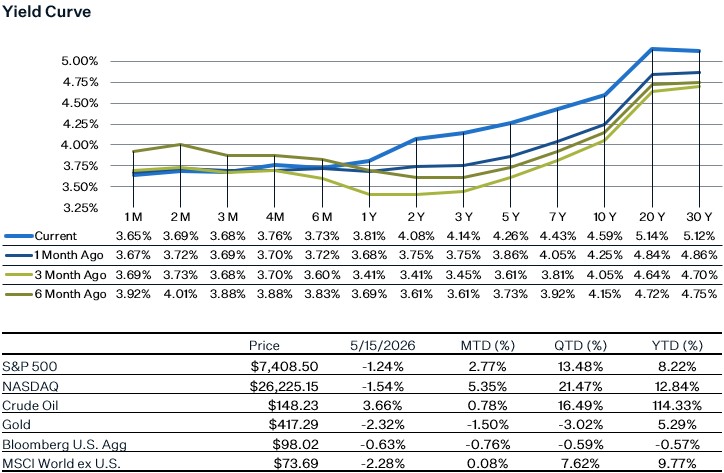

Market Update

Despite markets reaching record highs last week, several economic data points caused investors to reassess the path of the U.S. economy. Stocks rallied mid-week as optimism surrounding the Trump-Xi Beijing summit boosted sentiment, with the S&P 500 closing above 7,500 for the first time on Thursday, as investors largely looked past a hotter inflation print. However, as the summit wound down without any meaningful resolution or major business agreements, markets began to reconsider the outlook, particularly around the risk that the Strait of Hormuz could remain closed longer than expected, keeping inflationary pressures elevated. During the week we got two inflation readings (CPI and PPI) that both came in hot, especially the PPI. Despite retail sales for April coming in line with expectations, affordability concerns sparked a sell off in certain consumer and retail names – with the consumer discretionary sector underperforming and ending the week down 3%. By Friday, bond prices sold off, pushing the 10-year Treasury yield toward 4.6% as investors increasingly priced in the possibility of another Fed rate hike by year-end, despite the Senate having confirmed Kevin Warsh as the next Fed chair. During the week, equity leadership remained narrow, with AI and semiconductor-related names continuing to drive the rally. NVIDIA reached a new all-time intraday high, while Cerebras Systems surged 68% following its IPO debut. Looking ahead, NVIDIA’s Q1 earnings next Wednesday will likely be the most important near-term catalyst for AI sentiment and the broader market.

What Inning are we in for the AI trade?

The honest answer is that no one knows. Most investors believe the AI trade has enormous room to run over the medium term and the bull case rests on the thesis that token consumption is expected to grow 24x by 2030, driven by a shift from episodic chatbot use toward an always on agentic AI that constantly runs across consumer and enterprise applications. Hyperscalers are investing accordingly, and the economics are improving with token costs falling more than prices mainly due to custom chips.

On the semiconductor side, the numbers are striking. The SOX index is up approximately 70% since late-March lows, and semiconductor EPS estimates have been revised upwards by more than 25% year-to-date. The price move is well in excess of the revisions, implying that the market has priced in plenty of optimism. The caution in the AI complex comes more from positioning and price relative to fundamentals in the near term. Hence, a correction, might be the healthiest thing for the durability of the trade. But, if one is forced to pick an inning, a combination of late inning for infrastructure and early inning for the adoption cycle would put us somewhere in the middle of the game.

April CPI Inflation Report

Inflation accelerated again in April, led by higher energy prices. Headline inflation increased 0.6% month-over-month, bringing the year-over-year rate to 3.8%, significantly higher than the 3.3% pace in March and the highest headline number we’ve seen in almost three years. Energy prices rose 3.8% in April, led by higher gas prices which increased 5.4% (gas prices are now up 28.4% from a year ago). We’re starting to see food prices increase – with food at home increasing 0.7% for the month (highest monthly increase since August 2022). Fertilizer prices have significantly increased since the war began, and farmers will soon have to buy fertilizer for the fall planting season at the current elevated prices. This could cause more upward pressure on food inflation in the coming months.

Core CPI increased 0.4% month-over-month (year-over year 2.8%). Shelter increased 0.6%, although most of this strength was due to the government shutdown which caused data collection disruptions - so the jump in shelter is likely a one-time thing. Lodging away from home rose 2.4% for the month, as hotels and other accommodations likely passed on some of the higher operational costs (electricity for instance increased 2.1% in April). We also saw another large rise in airfares - up 2.8% for the month. Bottom line: April’s report supports the notion that the US-Israel/Iran war impact on inflation isn’t just higher energy prices. Higher energy costs can ripple through the broader economy, as most businesses rely on energy to manufacture products and run their day-to-day operations.

Retail Sales & the Consumer

U.S. retail sales rose 0.5% in April, marking a third consecutive monthly gain, though beneath the surface the data tells a more fragile story. Retail sales are not adjusted for inflation, meaning much of the increase reflects higher prices rather than stronger consumer demand. Gas station receipts alone rose 2.8% as the Iran conflict pushed fuel prices to their highest levels since 2022, while grocery spending also increased amid rising food costs. Consumer resilience remains concentrated among higher-income households, supported by the continued equity market rally, while tax refunds in March and April came in more than $20 billion per month above last year, temporarily offsetting the roughly $10 billion monthly increase in gasoline spending caused by the energy spike. However, underlying trends remain weaker as inflation-adjusted wage growth continues to decline, savings rates are falling, and consumer sentiment remains near record lows. Bottom line: if the conflict persists for much longer and fuel prices remain around current levels while the tax refund tailwind fades, household spending could begin to soften more broadly in the coming months.

Sources:

https://markets.jpmorgan.com/jpmm/research.article_page?action=open&doc=GPS-5304353-0

https://www.bls.gov/news.release/pdf/cpi.pdf