Markets are showing optimism, though the Fed remains hawkish and is likely to get more hawkish.

On the Verge of Change: Summary

- U.S. stocks continue to climb the wall of worry: As the threat of continued rate hikes hang in the air, the economic outlook continues to look less and less gloomy, pushing stock prices higher.

- International stocks are bouncing back from the gloomiest of expectations: However, the bright outlook is tempered by the likelihood that further rate hikes strengthen the dollar and eat away at international gains for U.S. investors.

- The U.S. yield curve remains unsustainably inverted: Assuming we do not have a significant round of rate cuts at the end of the year, the long end will have to rise at least 75 bps if not further, causing a lot of long duration pain to investments with long duration exposure.

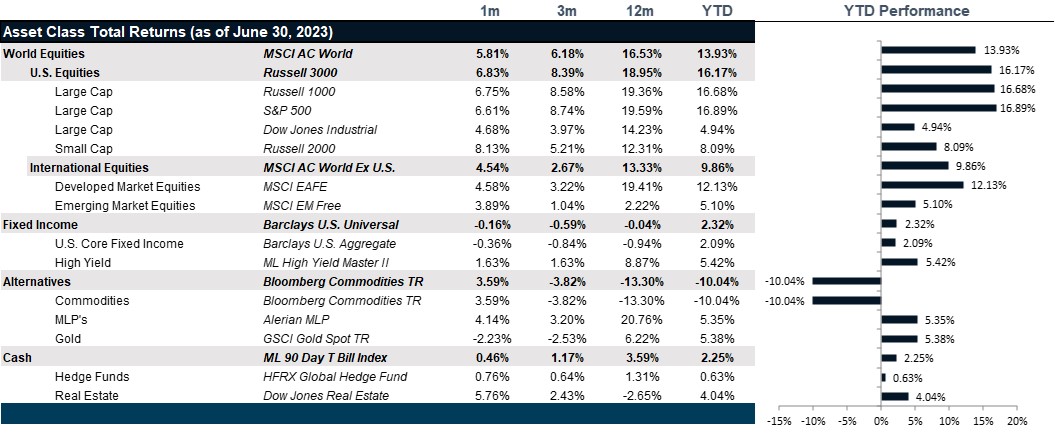

Market Performance as of June 30, 2023

Market Review: U.S. Optimism vs. European Pessimism

Equity markets in June posted positive returns, reflecting greater optimism as inflation eased and policymakers resolved the debt ceiling crisis. The S&P 500 ended the month up 6.6%, with consumer discretionary, materials, and industrials sectors contributing to most of the gains. The utilities sector, in contrast, was the main laggard. The Dow Jones Industrial Index posted a 4.7% return, the Nasdaq was up 6.7%, and the Nasdaq 100 up 6.6%. The information technology sector started rallying earlier in the month with Nvidia and AI getting most of the attention, but ended up giving back some of the gains. Breaking the trend from previous months, large cap stocks underperformed mid and small cap stocks. Inflation eased in line with expectations at 4.0% year-over-year, and 0.1% month-over-month, as the energy index declined 3.6% in May. Core CPI, however, remained stubbornly high, with shelter costs the largest contributor. After 10 consecutive interest rate increases, the Federal Reserve decided to leave the target range for the federal funds rate at 5% to 5.25%. They are putting more weight on the strong employment data and sticky core CPI, and communicated additional rate increases to come.

European stocks ended the month mixed at 2.43% after giving back the gains made in the first half of the month on worries that further interest rate hikes might cause a recession in Europe. Although inflation in the Eurozone decreased to 6.1% year-over-year, core inflation remained stubbornly high according to the European Central Bank. They raised interest rates by 25 bps to 3.5% and expect more interest rate hikes to come in the next months. The UK’s FTSE 100 posted a 4.1% return. The inflation rate in the UK remained unchanged at 8.7% in May, but core CPI rose to a 31-year high of 7.1%. The Bank of England unexpectedly raised interest rates from 4.5% to 5% to tackle stubborn inflation. Japan continued its strong year-to-date performance with a 7.7% return, supported by loose monetary policy and corporate reforms. Inflation in the region slowed to 3.2%, still above Bank of Japan’s 2%-target.

Emerging markets reversed course from May with the MSCI Emerging Market Index returning 3.8% in June, and the Latin America region posting a strong return of 12.1%. Wall Street banks are cutting China’s growth outlook for the second quarter after a very strong beginning of the year, as the reopening effect is running out faster than anticipated.

The U.S. bond market remained mixed on varied economic data with Treasuries posting a return of -0.75% for the month. The 1-month and 3-month yields declined to 5.11% and 5.28% respectively. The 2-year and 10-year yield rose to 4.89% and 3.84% respectively. The U.S. bond market in general returned -0.36% while global bonds were modestly down -0.01% in dollar terms. Although fears over a recession in the second half of the month pushed yields lower in the Eurozone and UK, bond markets fared worse in June with euro-denominated and sterling-denominated bonds posting returns of -0.33% and -0.70% in euro and sterling terms, respectively.

Commodities had a strong month with the Bloomberg Commodity Index returning 4.0%. Precious metals, however, declined 1.15% as inflation has steadily fallen. Oil prices jumped earlier in the month as Arabia Saudi announced it plans to reduce exports but ended flat with WTI and Brent at $70.64 and $75.68 a barrel, respectively.

Going Forward: On the Verge of Change

A core of economic theory is notion called “ceteris paribus” which effectively means “holding all other conditions constant.” When testing marginal effects, that notion is important. However, in real life, the pandemic seems to have acted as a catalyst that has ushered in many changes all at once. So many conditions we have grown used to are changing so profoundly that looking forward feels like an overwhelming exercise of “what if’s.” Let’s think about the big themes that are changing. First, globalization was tested during the pandemic only to discover a far more fragile supply chain than we had otherwise assumed, marking the peak of globalization. This reversal of offshoring has been a boon for the rebuilding of middle America but has ushered in longer term expectations for permanently higher inflation than we have gotten used to over the last three decades. This, in combination with Russia’s invasion of the Ukraine drove inflation to multi decade highs, marking the first real Fed imperative to reverse over two decades of ultra-low to normalize at a level of interest rates we have not seen since just before the Great Financial Crisis (GFC), which was the last time the Fed tried to break corporate America’s dependence on low interest rates. Beyond the big macro themes, there are plenty of other changes happening, such as downward pressure on margins resulting from higher wage growth, downward pressure on earnings multiples resulting from higher interest rates and pressure on balance sheets resulting from the highest level of indebtedness in history. And, though we can’t tell the future, we do know one thing: markets hate the uncertainty that comes with change.

Stocks Climbing the Wall of Worry

All that said, equity markets seem to be climbing the wall of worry with margins stabilizing after being hit hard in 2022 with inflation. As inflation fell from a high of 9.1%, a level not seen since 1981, margins stabilized with wage inflation now the largest contributor to inflation. In addition, wage inflation at 6% is now growing faster than the consumer price index at 4%, as of the end of May, the last official print, and this has driven up buying power. Though earnings growth has been slowing, revenue growth has been straight up. And, even with some of the strongest performance since before the pandemic, the valuation of the equity market is only modestly higher than its long-term fair value. However, the devil is in the details. At the sector level, many opportunities present themselves. At the stock level, even more opportunities abound. With economists continuing to downgrade the expected impact of the coming slowdown, equity markets are looking past the recession as if it will have no impact at all. While the slowdown may indeed be a “non-event,” there are still risks to the downside after the performance we have recently experienced. We view these risks as balanced for equity.

The International Quandary

While the U.S. opportunity looks bright, the developed international opportunity looks brighter, but largely because developed international stocks are very fast to assume the worst possible outcomes. No one ever expected any growth out of Japan. No one ever expected Germany to overcome its reliance on Russian oil. No one expects anything from the U.K. since Brexit. Meanwhile, all three regions have managed to outperform terrible expectations, but when compared against U.S. performance, taking into account shifts in the dollar resulting from a very fast Fed reaction compared with the ECB, BOE and BOJ, all three equity markets have lagged U.S. stock performance. However, with so much good news priced into U.S. equities, one could make an argument for international exposure. Much will depend on the outlook for the dollar. If the Fed does not cut rates, the dollar will remain strong and diminish the value of investments abroad. Though, the outlook for Japanese growth remains attractive on the whole. In emerging markets, no one expected the Chinese reopening to fade so fast and we don’t see much to be excited about in the second half of the year, with a sober Chinese outlook and a sober commodities outlook on the back of global slowdown.

The Unsustainable Yield Curve Inversion

The yield curve remains persistently inverted which cannot last forever, lest the entire banking system in the U.S. go bankrupt from paying higher rates on deposits than they can collect on loan yields. Either bonds will have to accept a brighter economic outlook with a higher inflation experience to make up for it, and see the long end of the curve rise up to meet those expectations, or the economy will break under the weight of its indebtedness and the recession will be deeper than currently forecast. While the truth will likely lie somewhere in the middle, we anticipate that the corporate balance sheet is healthy enough to withstand higher interest rates such that we should not see a slew of defaults. This leads us to favor the first scenario more with the risk to the long end of the yield curve more at risk than default rates. This offers both opportunities and risks with opportunities in higher quality corporate debt and the risks to longer dated debt.

Net View

We remain balanced in our view of equity risk with the U.S. equity outlook, though large cap stocks look more attractive in a growth slowdown. Within international equities, Japan looks more attractive than Europe and emerging market equities are least attractive. Finally, within bonds, we maintain an overweight to high-quality, investment grade corporate bonds.