Markets have moved toward a soft landing narrative, but risks remain and will likely fuel volatility.

Soft Landing or Bumpy Ride?: Summary

- The soft landing narrative seems to have taken hold: revisions to GDP suggest that we have avoided a recession, and corporate earnings are beating expectations.

- The case for weakness is equally compelling: the weakness of the consumer in combination with sticky inflation could prove a recipe for additional volatility.

- The case for volatility remains strong: geopolitical conflict and bitter politics could outweigh a good earnings season with both influences ensuring that the markets will be volatile.

Market Review: Shifting Expectations

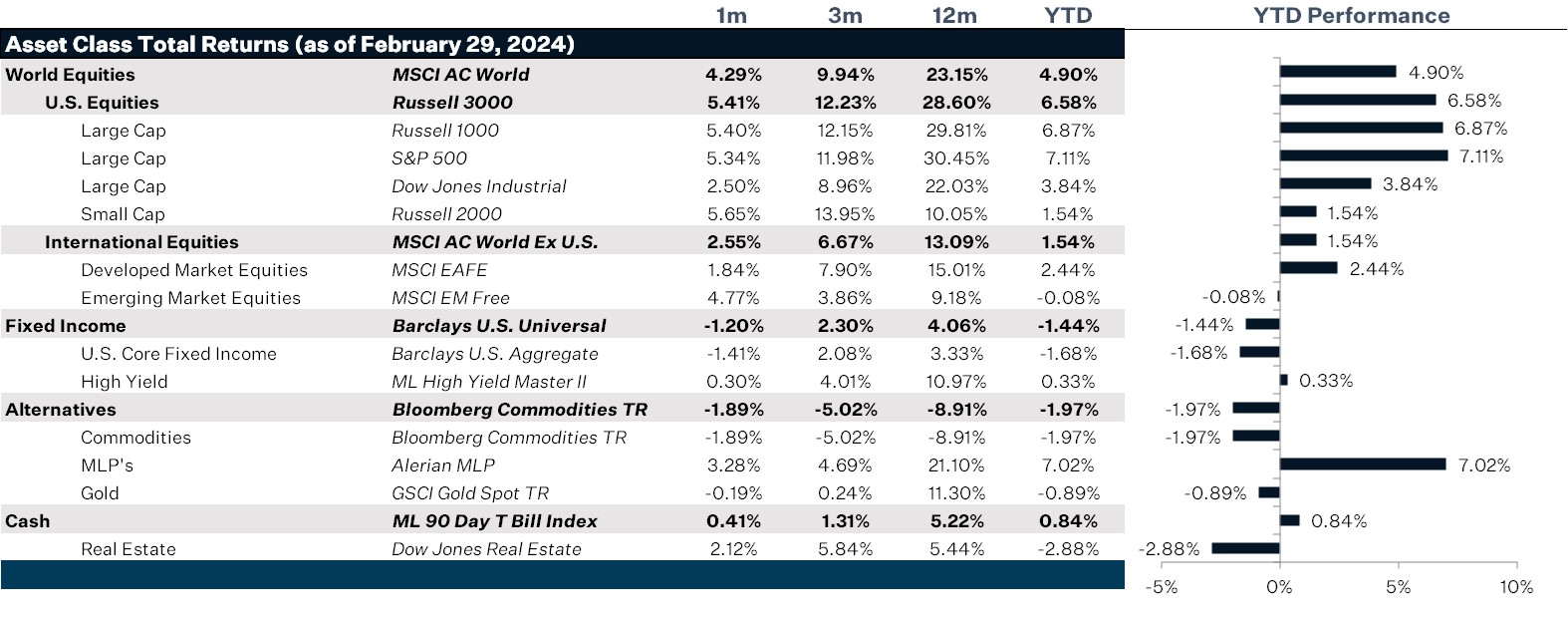

As economic revisions continued to trend up for 2024, the concerns about recession have largely been erased and U.S. equity markets have reflected the optimism in a blockbuster month, up 5.34% in February for large caps. Much of that performance was driven by a resurgence of growth performance consistent with optimism, which turned in a 7.3% performance versus 3.05% for value. Mid cap stocks also performed well at 5.93% with small caps lagging at 3.32%. That said, optimism for small caps built up over the month as the consensus for growth shifted.

International equities were hit by a moderately strengthening dollar over the course of February and that impact was far worse for European equity where economic expectations remain somewhat stagnant. European equities returned 1.49% in dollar terms, slightly behind the overall MSCI EAFE Index return of 1.86%. Japan remains the favorite in international investing, returning 2.91% in dollar terms. Emerging markets also turned in a strong return as China bounced this month with a 6.9% return versus 3.26% for the MSCI Emerging Markets Equity Index.

Another major shift in expectations took place in the Fed Funds Futures, now pricing in three rate cuts in 2024, in line with the Fed Dot Plot. In addition, the upward revisions to growth seem to have pushed the long end of the yield curve up, resulting in losses across the bond universe. Only high-yield credit debt bucked this trend while asset-backed credit was relatively flat as default expectations eased and the spread over treasury bonds fell, reflecting the lower risk expectations.

In real assets, commodity indices flagged in February. Though oil prices rose modestly over the month, the move was not enough to satisfy the expectations already priced into the futures curves. Precious metals and industrial metals also performed poorly, the former in response to waning inflation trends. However, industrial metals performance was a surprise as it is generally correlated to revisions in expectations for economic activity. Agriculture took the biggest hit this month as supply is looking to outstrip demand this growing season.

Going Forward: Soft Landing or Bumpy Ride?

The markets went from flux to full speed ahead. In the space of a few weeks, economists dramatically revised expectations for 2024 up to 2.1% for the full year and revised 2025 expectations down modestly, suggesting a very mild slow down to 1.7%. Meanwhile, expectations for the Consumer Price Index were revised down and then back up again for both 2024 and 2025, now currently at 2.7% and 2.4%, respectively. This suggests that investors are pricing in a soft landing while still conceding that inflation remains sticky. Expectations for Fed cuts have fallen into line with the Fed Dot Plot with Fed Funds Futures now pricing in three rate cuts in 2024 starting at the June meeting. The Fed has repeatedly communicated their willingness to be cautious before cutting rates to ensure that the inflation genie is indeed back in the bottle. The continued concern around inflation supports the “higher for longer” interest rate narrative that would accompany a slow reduction of rates. That said, unemployment is continuing to rise while wage growth continues to fall, setting up for the slowdown in growth expected in 2025. However, if the slowdown comes faster or inflation lingers for longer, the soft landing scenario may evaporate into a cloud of volatility.

The Case for Growth

Although wage growth is slowing down, it is still growing in real terms after accounting for inflation. Hourly earnings grew at 4.3%, year-over-year at month end while CPI grew at 3.1%, year-over-year. Assuming the growth narrative is right, then the S&P 500’s forward price-to-earnings ratio of 21x on a market-weighted basis and 17.7x on an equal-weighted basis could continue to expand. The breadth of the rally is starting to expand and the nature of the rally has moved toward higher-quality stocks with upward earnings revisions and stronger balance sheets. However, the yield curve is not set up for this with a long end that remains stubbornly too low. If this soft landing were to come to pass, we would have to see more of a lift at the long end to reflect the overall rosy expectations. The long end has so far moved down this month, not up, and this leaves the bond markets at risk of further pressure. All that said, the recent hiccup with NVDIA, whose blowout earnings reinvigorated Ai optimism, seems to have created a spark of upset in the equity markets, suggesting the yield curve outlook may be more correct.

The Case for a Cold Shower

The challenge to the case for growth is that it rests solidly on the consumer and the wage growth story. The challenge there is that consumers have spent well in excess of their pandemic savings and wage windfalls and have racked up significant levels of credit card debt, which at current interest rates carry hefty interest costs. Not only are credit card debt levels up, but 30-day and 90-day delinquencies are also sharply up, suggesting that consumers are getting out beyond their skis. Though not yet at the extreme levels experienced during the Great Financial Crisis (GFC), we are seeing levels at the top of the range established post-GFC. To make matters worse, the hotter-than-expected Producer Price Index read for January could be a canary in the coal mine for a hotter Consumer Price Index and the potential for the Fed to continue to push off the beginning of rate cuts. If the overstretched consumer starts to slow with no support from the Fed, the much-dreaded R word could come back into the mix.

The Case for Volatility

Like most things, the answer may lie somewhere in between the best and worst scenarios. However, the pressure for upside and downside outcomes comes from many directions, suggesting that regardless of the end destination, the journey could be bumpy. Upside pressure is primarily backward-looking but does impact sentiment greatly through the string of solid earnings, particularly across retail as we have seen. NVDIA aside, the outlook and momentum for AI does not seem to be abating and is very likely to be transformational over time, which may support further expansion than what seems rational at the moment. To the downside, we continue to see conflict, politics and looming regional bank crisis as sources of tail risk. Though hardly making headlines, Congress quietly passed yet another continuing bill to avoid a government shutdown. This has become overly normalized, and given the bitterness of U.S. politics, the potential for a disruptive political showdown going into the election is a distinct possibility. What could really upset the apple cart would be the commercial real estate debt sitting the regional banks desperately awaiting rate cuts that may be delayed, which could kick off a more significant bout of volatility.

Net View

The revised outlook for growth leaves us with a neutral portfolio view while our expectation for continued volatility supports hedging equity risk assets.