The markets are priced for a soft-landing, but we think it could be a bumpy ride.

A Picture of Vulnerability: Summary

- The Santa Claus Rally has left equities priced for rate cuts: if the Fed so much as blinks, the market volatility will erupt.

- The inverted yield curve is so 2023: either we are headed for a recession complete with a Fed rate cutting cycle or the outlook is much better than expected, but the inverted yield curve cannot continue.

- Tail risks abound: if the frozen war in Ukraine was not enough, the Gaza conflict, rising piracy on the high seas, increasing trade tensions in China, and a contentious election year in US with elevated political risk all represent tail risks in the coming year.

Market Review: Year in Review

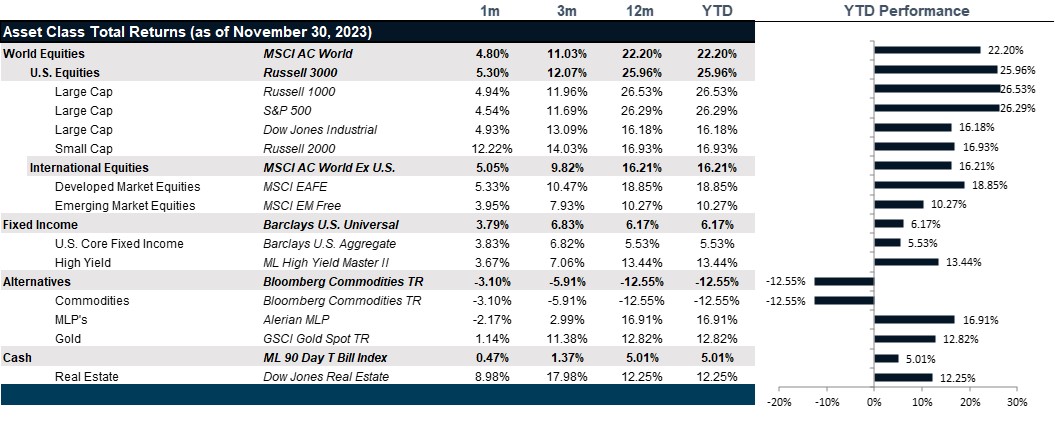

2023 was a turning point. Inflation fell throughout the year while the contribution of energy inflation went negative early in the year as Europe and the world quickly weaned themselves off Russian oil, reducing the impact of the ongoing war in Ukraine. However, unemployment remained steadily low and wage growth has remained steadily higher than the historical average. That presented a conundrum for the Federal Reserve, who felt compelled to continue to raise rates steadily until the July meeting. Meanwhile, expectations for year-end 2023 GDP growth, which started the year at near recession, were steadily revised up and expectations for year-end 2024 GDP growth were revised down for the first half of the year before taking an about face and being revised back up to a mild slowdown by year end. This effectively splits the year into two distinct halves: the first half, when the Fed was still raising rates and the market expected a recession and the second half, when the Fed finally hit the pause button, though repeatedly threatened to continue to hike rates. By the second half, fears of a recession had all but dissipated even in the face of a horrific attack on Israel and continued war. Growth expectations were upgraded to a mild slowdown, though 2024 was largely still expected to be slower than 2023.

In the midst of these revisions in expectations, stocks, meanwhile, steadily looked past any concerns about a slowdown and continued to assume that rate cuts were, in fact, in the cards. Price-to-earnings multiples, both on a trailing as well as on a forward basis, found their footing and, despite higher rates, began to steadily climb, all but pricing in strong rate cuts while at the same time assuming a continued recovery in earnings growth. The year ended up 26.34% on a total return basis. U.S. equity markets did experience two significant drawdowns, first in February as the specter of continued inflation reared its ugly head in the form of a nasty surprise and again in July, August and September as oil prices rose dramatically, reigniting concerns that the hiking cycle would resume after the July pause. However, by October, oil prices fell and continued to fall for the remainder of the year, making the Fed Funds rate pause feel more permanent. And the Santa Claus Rally took us into the New Year.

International equity markets also had strong performance with the MSCI EAFE index turning in 18.95% over the year, with Japan as the clear winner with a 29.03% total return in US dollar terms. Within the equity space, emerging markets was the lack-luster performer with only 10.12% total return for the year, spread between China losing 11.01% for the year and Latin America gaining 33.57% for the year.

Despite equity market participants pricing in a decidedly rosy picture where growth only slows mildly, earnings continue to improve and rates miraculously fall, bond market participants have stuck to their bearish view. The unsustainably inverted yield curve has remarkably sustained the entire year with neither end making a move to meet the other. The short-end remaining high because the slowdown in growth hardly seems like enough to justify the seven rate cuts that are priced into the markets and the long-end because they hardly see 1.3% GDP growth as anything worth pushing the long end above the 4-4.2% range it has oscillated in all year. Bond markets largely had three segments to the year. The first half was largely upward in trajectory with the market oscillations generally pushing yields down as the Federal Research finally approached a pause in July. The fall was rather ugly across the bond markets also, as they began to price in a hawkish Federal Research view and higher-for-longer view for interest rates across the board. Finally, the fall rally where investors piled into bonds, pricing in a soft landing; a stronger credit outlook and returns for high-yield were particularly robust. The full aggregate bond index returned 5.53%, with treasuries returning 4.05% for the year, mortgages returning 5.05% for the year, and investment-grade bonds returning 8.52% for the year. Though not included in this index, it is also worth noting that high-yield debt returned 13.45% for the year as downgrades outpaced upgrades almost two-to-one.

In the real assets space, commodities predictably performed the worst, losing 12.55% in aggregate and losing 25.59% in the energy subindex. Meanwhile, REITs performed better than expected with the broad REIT index returning 9.07% and returns across the sub sectors ranging from 3.16% for office REITs to 22.93% for hotel REITs. Industrial warehouses returned 19.71% while shopping centers came in middle of the pack with 9.27% return, and apartment REITs came in at 6.56%, despite significant upward revision in rents.

Going Forward: A Picture of Vulnerability

The year ended with a moderating view of risk and an improving outlook for growth. However, it also ended the year with seven interest rate cuts largely baked into equity pricing and into the yield curve. If seven rate cuts did come to pass, the yield curve would no longer be inverted, and the long-end wouldn’t have to suffer any pain. Equities would even look cheap from here. Commodities would look ready to recover and real estate would settle with the exception of office space where the bloodbath is still in the works. In fact, so many good outcomes hinge on just one assumption and that assumption hinges on the outlook for inflation. We must consider what might come to pass to deliver a challenging inflation picture.

Inflation

Despite conflicts near energy producing hubs, oil prices have remained a negative contributor to inflation, falling all year as demand has fallen. Though the first inflation print of 2024 showed a higher-than-expected number, it was not alarming enough to change market assumptions of up to six rate cuts. Wage inflation has been the slowest moving component of inflation and continued trade tensions with China will almost certainly keep demand for onshore jobs high and keep wages high. In addition, demographics continue to work against this sudden desire to reignite the domestic manufacturing apparatus. Labor participants in the 25-54 age group are now employed at an 83% participation rate, which is at the very high-end for the cohort, suggesting near full employment. To add to the pressure, the potential for rising costs to ship commodities, chemicals and goods could spike amidst a spate of maritime piracy may be the short-term fly in the ointment to cause the Fed to blink. Also, keep in mind that it does not require the Fed to raise rates in order to undo market valuations, it only requires them to cut less than expected. If inflation remains above 2.5%, we could be faced with a Fed unwilling to tempt inflation fate.

Growth

Global growth expectations continue to improve, and this has largely been priced into equity earnings expectations. The big question in the minds of most economists is: is the higher cost of capital truly priced in? In reality, this tends to hit the economy at a lag. High-yield debt is issued at maturities that are four to seven years out. So, it takes time for higher rates to rob companies of buying power. In the consumer space, it will generally hit within 12-24 months as the cost of credit card balances will almost certainly crimp household spending. However, with mortgages finally falling and residential rent indexes falling precipitously, the household balance sheet may escape the need to truly pull back on their balance sheet immediately. This could set us up for the goldilocks scenario that is priced in. However, sentiment will play into this story and regardless of what side of the aisle you associate with, politics plays into sentiment. Political risk in the U.S. is rising, is more contentious than ever, and could distort reality enough to cause unforeseen outcomes which could be worth monitoring.

Risk Appetite

With equities priced for perfection and bond yields well above dividend yields, why would investors take risk at this point? The opportunity for upside will now lie in structuring yield and understanding and taking advantage of volatility and dispersion through derivatives, options and (wait for it) hedge funds. With fee compression and greater access, the long-hated asset class may finally come back into its own. That said, derivatives and well-designed option strategies may do just as well for investors.

Net View

Equities are less attractive in a higher-yield environment, leading us to prefer both high-grade and high-yield credit as a way to benefit from corporate strength while minimizing equity volatility. We see opportunities overseas in emerging markets as the dollar could remain weak if rates do fall, even modestly. Across the portfolio, we expect greater volatility this year, making options potentially more expensive, but still worth considering.