Market Update

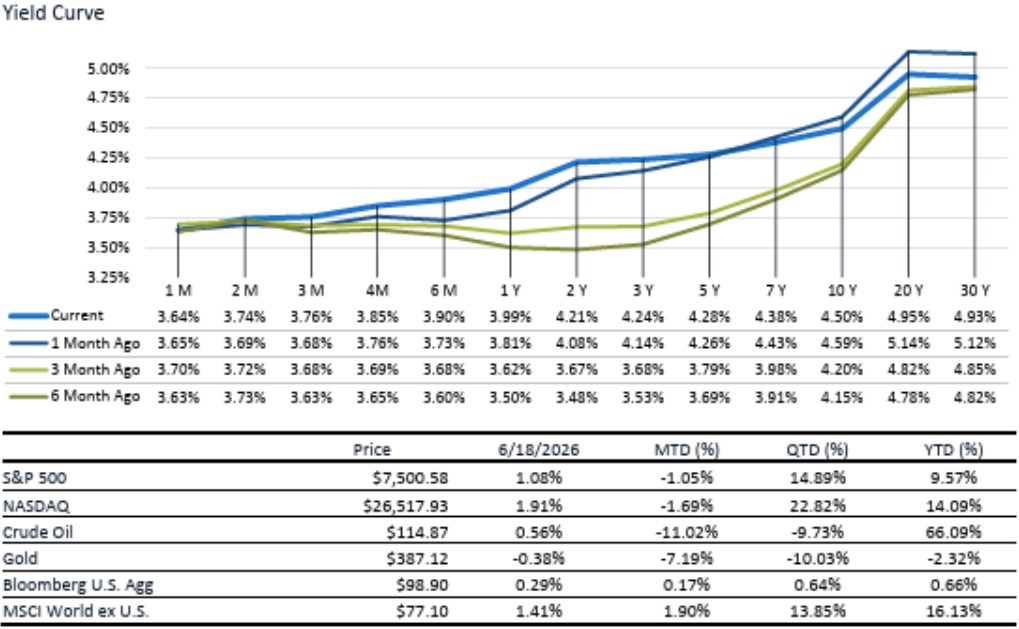

Two events drove markets last week. The most significant was the US and Iran peace agreement. While the deal remains in flux, markets quickly priced in a resumption of Strait of Hormuz flows, with WTI crude oil ending the week down over 10% and the average price of U.S. gasoline falling to below $4/gallon. Midweek, however, sentiment weakened after the Fed struck a more hawkish tone than expected. While rates were left unchanged, the Summary of Economic Projections showed higher inflation forecasts, and 9 of the 18 participants now expect at least one rate hike in 2026, with 6 members forecasting two or more hikes. Additionally, Fed Chair Warsh announced five new Fed task forces - suggesting that Warsh is beginning a broader review of the Fed’s operating model, which could eventually lead to changes in the dot plot, the balance sheet framework, and how the Fed uses real-time data among others. Short-end yields increased notably after the FOMC meeting on the back of higher near-term rate expectations. On the consumer side, spending remains resilient despite higher gasoline prices. Retail sales rose 0.9% in May, while sales excluding gas stations increased 0.7%, indicating that households continued to spend even as fuel costs moved higher. Part of that strength was supported by tax cuts and lower withholding that boosted disposable income earlier this year. Looking ahead, lower gas prices should provide some relief, but the tailwind from those tax benefits is likely to fade, which could lead to subdued spending growth in the second half of the year.

June FOMC Meeting

The Federal Reserve left the federal funds rate unchanged at 3.50% to 3.75% at last week’s meeting, with the decision supported by a unanimous 12–0 vote. The dot plot was the main focus as it came in much more hawkish than expected, with 9 out of 18 Fed officials projecting at least one rate hike for 2026 and 6 members looking for two or more hikes. Only one member forecasted a cut, and Chair Warsh chose not to submit a projection, consistent with his skepticism of the SEP’s current structure. The median Fed Funds rate also increased 50 bp in 2027 (up to 3.6%) and 30 bp in 2028 (to 3.4%). The more hawkish sentiment came from their updated inflation expectations. The main change to their economic projections was the increases in inflation numbers – bringing their 2026 headline PCE number up to 3.6% from 2.7% and increasing core PCE to 3.3% from 2.7%.

Perhaps the biggest development and takeaway was the creation of five Fed task forces – 1) Fed communications, 2) balance sheet policy, 3) data sources, 4) productivity and jobs in an era of technological change, and 5) inflation frameworks. The communications task force could propose some changes to the Summary of Economic Projections, along with fewer explicit signals about future policy decisions. This would effectively give the market less visibility into the Fed’s thinking around their next policy moves. The data task force is an interesting one and perhaps the one that could have severe implications for monetary policy going forward. This could result in the Fed incorporating higher-frequency and more alternative private data into their models, which may make policy more responsive to real-time shifts in the economy but could also make them sensitive to noisy short-term signals. Overall, it seems that Chair Warsh is beginning an extensive review of the Fed’s operating model, which could result in some notable changes to their current framework and how the Federal Reserve makes, communicates, and implements monetary policy.

May Retail Sales

Headline retail sales figures for May came in higher than expected, rising 0.88% month-over-month (MoM), versus economists' expectations of 0.60%, marking the fourth straight month of increases in the figure and rising 6.90% year-over-year (YoY). Unsurprisingly, gas stations led all categories, rising 3.40% MoM, but even after stripping out volatile inputs such as gas and auto sales, retail sales still grew 0.53% MoM, showing genuine demand growth. Increases were broad-based, with 11 of the 13 categories positive, and notable categories included nonstore retailers increasing 1.5% on the month and miscellaneous store retailers increasing 2.3% on the month. Notable decliners for the month were food service & drinking places and electronics sales, both declining by 0.1% and 0.5% MoM, and furniture was the only category negative on a YoY basis, coming in at -1.20%. The story here shows that the consumer remains resilient even amid the volatility from the conflict, as shown by the figures from both store and nonstore retailers; however, it should be noted that information from large card providers continues to show there is some fraying among cohorts, with higher-end consumer growth increasing at a much faster pace than lower-end consumer growth. Meanwhile, the weakness among decliners continues to show that the Middle East conflict has slightly dented consumers' willingness to purchase some discretionary items, especially as higher energy costs have likely crowded out some of that spending. Put together, the report paints a picture of a robust consumer who has been able to withstand geopolitical uncertainty and higher energy prices, but as tax tailwinds ease, the Kshaped economy shows few signs of narrowing.

Sources:

https://www.census.gov/retail/sales.html

https://www.federalreserve.gov/monetarypolicy/files/fomcprojtabl20260617.pdf https://www.federalreserve.gov/mediacenter/files/FOMCpresconf20260617.pdf https://www.federalreserve.gov/monetarypolicy/files/monetary20260617a1.pdf