Markets have not yet priced in the very strong likelihood of higher for longer interest rates.

Higher for Longer: Summary

- Equity volatility is here to stay: while the equity markets continue to focus on the end of rate hikes, we still believe that the market has not yet priced in higher for longer rates.

- The inverted yield curve is unsustainable: the long end of the yield curve is currently not fully reflecting the likelihood of a higher short end, nor does it take into account the more persistent elements of inflation that are being driven by longer term drivers like de-globalization or demographics.

- The effects on the real economy are overall positive: the effects of higher returns on savings combined with higher real wage growth will have a strong positive effect at the real economy level.

Market Review: Summer Vol

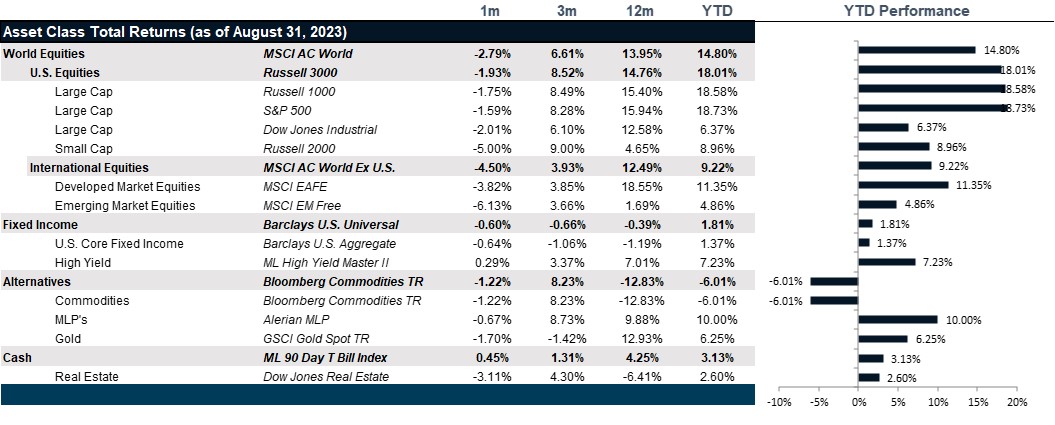

The strong advance in U.S. equities this year stalled in August. At the lows, the S&P 500 was down as much as 4.66% from the July highs and the Nasdaq corrected over 6.66%, although both indexes ended the month down just 1.59% and 1.50% respectively. Enthusiasm around a resilient economy, easing inflation and AI was countered by global growth concerns and a sharp increase in longer-term bond yields. Volume this month was generally light because of the summer season, having probably accentuated the market’s swings. On the technology front, NVIDIA’s blowout results failed to ignite a sustained increase in U.S. stocks, a sign many analysts interpreted as a negative technical signal that the AI-rally is exhausted. However, U.S. equities regained some ground towards the end of the month on the back of soft economic data in a “bad news is good news” rally. Job openings fell by more than expected and a cooler ADP employment report bolstered bets that the Federal Reserve would be able to hold interest rates steady at their next meeting. In late August, Fed Chair Jerome Powell gave no clear hints of the future path of interest rates from his perch at the Jackson Hole Symposium.

European stocks had a negative month with the Euro STOXX 600 down 4.00% on the back of rising U.S. bond yields, China’s worsening economic outlook and prospects of a prolonged period of higher interest rates. Banks shares across Italy and the rest of the Euro Zone fell sharply after Italy announced a one-off 40% tax on banks’ windfall profits, although rebounded in the following days as the government said later that the levy would be capped at no more than 0.1% of their total assets. Despite these headwinds, the STOXX 600 index managed to avoid its worst monthly performance in dollar terms for this year as it ended up recouping some of the losses on improved sentiment. The Nikkei 225 index declined 3.89% over the month amid uncertainty over the Bank of Japan’s tweak to its yield curve control strategy in July and concerns about the broader implications of China’s macro issues.

Emerging markets reversed course from the previous two months with the MSCI EM Index returning -6.14%. In China, economic challenges have raised fears of a global crisis as the property market is currently experiencing a significant downturn, youth unemployment is at record highs and consumer prices declined in July for the first time in more than two years. Meanwhile, recent attempts by the government to support its markets have failed to produce a steady rally with the MSCI China Index posting a return of -8.97% in USD.

In August, yields on longer-term U.S. Treasuries rose while shorter-term yields remained more stable. The 10-year yield broke to a new high of 4.34% in mid-August, reaching its highest level since 2007. This jump may reflect a combination of persistent inflation and a “higher for longer” interest rate outlook. However, a planned increase in the note and bond offerings this month may have also contributed to the move up in yields. This increase in issuance underscored government borrowing needs just a few days before credit-rating agency Fitch downgraded U.S. credit from AAA to AA+, citing fiscal deterioration and a growing debt burden. The 10-year yield finished the month at 4.10%, and the 2-year yield remained almost unchanged at 4.86%. The yield on 10-Year Japanese government bonds continued to rise during August following the recent shift in the Bank of Japan’s yield curve control policy, moving as high as 0.68% and putting more pressure on global yields.

Despite China’s economic issues along with concerns that maybe the Fed is not done with hiking interest rates, oil prices have stayed above $80 a barrel with support from falling inventories and output cuts from Saudi Arabia and Russia. Precious metals had an overall negative month with a return of -2.13%. After gold prices had declined to five-month lows in early August, the yellow metal marked a firm recovery as weak business activity data around the globe bolstered bets that the Fed had limited margin to keep raising interest rates. Gold still finished the month down 1.70%. Concerns over China and growing impatience with additional stimulus measures from its government hit copper prices earlier in August. Despite signs of improving demand in the coming months, weakness in the dollar and China’s move to support its currency, Copper prices fell -5.45%. September Henry Hub spot prices for natural gas reached a near seven-month high of $2.92, but the market returned to mid-$2 levels as concerns about approaching fall weather and stubbornly high gas inventories have kept it from rallying.

Going Forward: Higher for Longer

As summers go, this summer was a good summer to be optimistic and bet against the Fed. The S&P 500 returned 9.34% since the end of May while bonds fell by 1.06% over the same period. Meanwhile, the real economy soldiered on with commodities turning in a strong 9.29% for the summer after losing over 13% from the start of the year until May and real estate REITs turning in 3.77% return for summer after losing just over 2% at the start of the year. However, given that we are now near or at the end of the hiking cycle and given that rates are expected to remain above 4.5% or possibly higher, who is more at risk?

Weak Equity Outlook

The weaker the data, the stronger the case for the Fed to end the biggest tightening cycle in the last two decades. However, what might normally have been significant rallies in anticipation of a return to greater liquidity, the rallies have been more subdued. Though 100 bps of rate cuts are priced into the Fed Funds Futures curves, most market participants accept that we are in a higher for longer interest rate environment. Given that assumption, equity markets still look overvalued at 20x price to forward earnings. Even taking into consideration the hefty 30% weight to Technology which is traditionally higher multiple in nature, the S&P could still take a significant hit to pricing when the Fed is slow to cut rates on the other side. So, the outlook for stocks may not be dire, but it is not rosy. Keep in mind that a 10% loss for equities is within a small correction to the multiple, but that can be overcome through healthy earnings growth over time.

Weaker Bond Outlook

Equity market psychology never fails to deliver. From the lowest position in the capital structure, these investors only get paid in the good times and by buying equities believe good times are always around the corner. This year is no exception. With a Fed pause hanging in the balance, the markets are taking a Pollyanna approach to reading the tea leaves. If the labor markets show signs of weakness, then surely the Fed will stop raising rates. While that may be true, this doesn’t necessarily mean the Fed will cut rates and support equity market pricing. Meanwhile, the debt dynamics of the heavily indebted U.S. government in a higher rate environment is not great news to bond holders. In a higher for longer scenario, bond holders make more yield for their investments, but prices are also unlikely to rebound to pre-Fed hiking levels. The pain that has yet to be felt in the long end of the curve to correct the inverted yield curve back to a normally sloped yield curve where the time-value of money is once again positive will have to be significant. All that said, these expected losses will be in the context of the risk of bonds, which is to say that a loss of 2-3% is very large for a bond holding if you are only going to make 4% in yield. However, once the correction in the yield curve takes place, there will be a lot of opportunity to make strong returns with much less risk.

Real Economy

The real economy, however, seems to be surviving in a Goldilocks tale of two worlds: the one the Fed is monitoring through inflation and labor data and the one where wage prices are growing in real terms and earnings have troughed out and are expected to improve from here. Though we remain concerned that the Fed will push the tightening too far and turn a mild slowdown into something worse, so far, the data seems to be softening at just the right moment with U.S. Manufacturing data back down below COVID levels, job postings falling and payrolls falling, we may thread this needle yet. However, the story is far from over and the economy is trundling along better than anyone expected given the blistering pace of the tightening. And, while the adjustment was swift and painful, the end result is likely to be far more positive in terms of real wage growth, real yields earned on savings at lower risk and real economic value creation. What will suffer in this scenario, however, are risky investments that required cheap financing or unrealistic multiples to entice investment. The market as we settle into the new normal seems likely continue to reward secular long-term themes and quality, but will continue to shy away from highly valued, high-risk plays.

Net View

We remain balanced in our view of equity risk with the U.S. equity outlook, though large cap stocks look more attractive in a growth slowdown. Within international equities, Japan continues to look more attractive than Europe and Emerging Markets equities are least attractive. Finally, within bonds, we maintain an overweight to high-quality, investment-grade corporate bonds and an underweight to long-duration bonds.