The Gaza-Israel Conflict will usher significant volatility.

The Fog of War: Summary

- The pain in the long end is only beginning: the long end of the yield curve must at least adjust enough to compensate for higher inflation in the long run and the Gaza-Israel Conflict’s impact to oil prices may exacerbate this in the near term.

- U.S. equity will have a leg up on international equity: as interest rates rise, the dollar will strengthen and U.S. investments will outperform international investments with similar fundamentals and, with the exception of Japan, the fundamentals also favor the U.S.

- How the Fed reacts to the conflict could either ease or compound the pain: because oil plays a central role in the immediate reaction, the Fed’s reaction could create further turmoil with further inflation-fighting hawkishness or help ease the market reaction if the economy is gripped by an oil supply disruption.

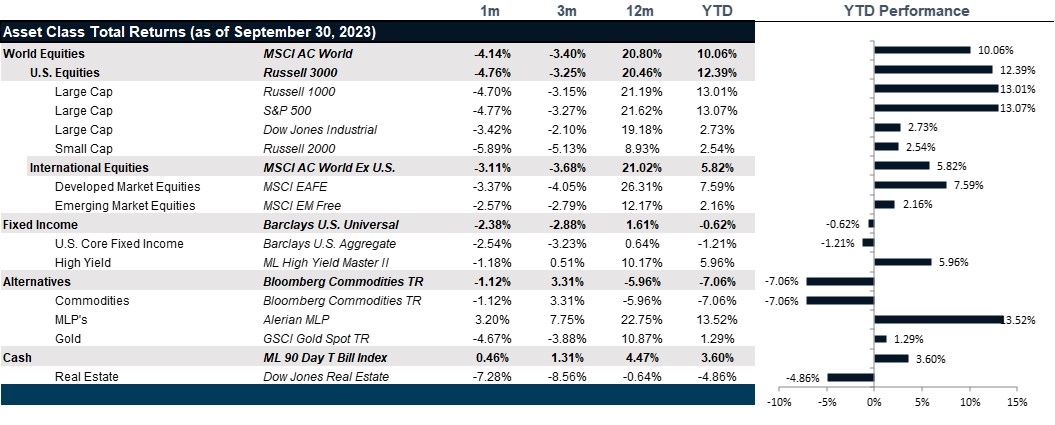

Market Review: An Ugly September

September has been historically the worst month of the year for equity markets and September 2023 was no different. The S&P 500 fell 4.77% and the Nasdaq 100 dropped 5.02%. The latest rise in oil prices has investors worried about the possibility of new inflation waves and higher for longer interest rates from central banks, spurring a sell-off in bonds which was partly to blame for the decline in equities. U.S. CPI in August rose 3.7% year-over-year because of soaring energy prices, slightly higher than the expected 3.6%, but core inflation, which strips out energy and food, dropped as expected to 4.3% from 4.7% in July. The Fed held rates steady this month in line with market expectations, but investors grew concerned as the Fed stiffened its hawkish stance amidst unexpected strength in the U.S. economy and the labor market. As the month wore on, uncertainty around a U.S. government shutdown may have also dented investor sentiment. Within the S&P 500, energy was the only sector to post a positive return. Real estate was the main loser as investors dumped cyclical stocks on concerns that tighter Fed policy will weaken the economy and overvalued tech stocks followed second due to their high sensitivity to higher interest rates.

European stocks followed suit with the Euro STOXX 50 returning -2.77% in euro terms and -5.11% in dollar terms amid concerns about a prolonged period of higher interest rates. The strengthening of the dollar compounded losses abroad. The European Central Bank raised interest rates by 25 bps to a record 4% as the fight against inflation took precedence over weak economic data. Flash figures showed that annual inflation in the euro zone had fallen to 4.3% in September, well below a 5.2% final reading in August. The U.K. fared better this month with the FTSE 100 returning -1.29%, driven by big oil-price gains and weakness in the pound. The Bank of England held rates steady at 5.25% following August’s inflation figures that showed the CPI falling below expectations to 6.7% year-over-year. The Nikkei 225 index declined 4.31% as concerns about China’s economic slowdown and uncertainty over the Bank of Japan’s tweak to its yield curve control policy persisted.

Emerging markets booked another down month with the MSCI EM Index returning -2.61% in September. A weaker-than-expected economic recovery and the lack of a large-scale stimulus package has negatively impacted the stock market in China for most of 2023. Bearish sentiment persisted this month as the MSCI China Index posted a return of -2.71%, but investors may have overreacted as the Chinese government has started rolling out a series of measures over the past weeks amid signs of stabilization in the economy. Consumer prices returned to positive territory in August and China’s factory activity expanded for the first time in six months.

U.S. Treasury yields continued to rise dramatically as fiscal concerns and worries over higher-for-longer interest rates explained severe losses in government bonds. The hawkish Federal Reserve policy update in September together with worries over the possible government shutdown sent yields to multiyear highs, with the 2-year and 10-year yields ending the month at 5.03% and 4.59% respectively. U.S. investment grade bonds declined 2.72% in September, marking the largest loss in seven months, and underperforming their high yield counterparts given their higher interest rate duration. European government bond yields also climbed as fiscal worries and the higher-for-longer narrative were not limited to the U.S. Following the recent shift in the Bank of Japan’s yield curve control policy to allow yields to rise more freely, Japanese government bond yields hit 10-year highs with the 10-year yield rising to 0.77%.

Oil prices jumped more than 30% over the past three months on the back of production squeezes by Saudi Arabia and Russia. Both countries reignited the rally in September after announcing that the voluntary cuts would continue until the end of the year, with both the WTI and Brent benchmarks reaching highs above $93 and $95 per barrel, respectively. WTI and Brent oil prices settled at $90.79 and $95.31 per barrel. The Bloomberg Dollar Spot Index rose 2.08%, hitting a 10-month high as the prospects for higher-for-longer interest rates sent investors to the safety of the dollar. Gold suffered significant losses as it lost the $1,900-an-ounce support, hit by the strength in the dollar and continually U.S. rising interest rates. The strength of the dollar and uncertainties around China’s economic recovery have also exerted pressure on copper prices. Copper futures are witnessing an extreme contango mainly induced by a decline in spot prices of 2.28%, suggesting a near-term over-supply. The surge in global copper inventories suggests weakening demand in the global economy.

Going Forward: The Fog of War

Herbet Stein once quipped, “If something cannot go on forever, it will stop.” Observe the action of the Treasury yield curve, which has been unsustainably inverted since December of last year, broadcasting a coming recession. Waiting for the recession to hit has been like waiting for Godot. Mitigating factor after mitigating factor kept this from being the worst recession in history, despite the most aggressive rate hiking campaign in recent history. However, the long end was slow to get with the rising rate program because rising interest rates are generally accompanied by hits to earnings (check), currency strength (check) and rising credit downgrades (check). While these are generally predictors of recession, we had many mitigating factors such as a huge pile of pent up savings racked up from mass fiscal support during the pandemic waiting to be spent as the economy reopened, a mass shortage of workers drove wages growth above inflation growth for the first time in decades and put cash in workers pockets, and three years of general pent up demand to make purchases, to be entertained and to travel. As the mass of printed money met with the forces of unleashed inflation brought forward by the pandemic and energy prices, the Fed acted decisively and should have crimped demand into a recession. But, so far, it has not materialized and the pressure on the U.S. balance sheet, burdened with extreme debt loads by any measure, are finally coming home to roost and the long end of the yield curve is throwing in the towel.

The Longer the Duration, The Greater the Pain

Let’s assume for a moment that the Fed Funds Futures curve is a reasonably accurate prediction of the Fed Funds interest rate in one year’s time. Then, it would suggest that the Fed will raise interest rates one more time and then cut interest rates four times in total, landing on 4.5% a year from now. If that is the case, then today’s 30-year Treasury yield of 4.86% is sufficient to restore yield curve normality. However, that is not enough to compensate long term bond holders for a potentially permanently higher rate of inflation, pushed by deglobalization and demographics driving up wages and final goods prices. If we expect that the Fed’s 2% target for inflation should be higher, say 3%, then anyone buying a bond for 30 years and only making 36 bps of extra yield is getting a raw deal because the pricing power of that coupon will diminish by 2-3% per year with just inflation alone. The longer the maturity of the bond, the more you must be compensated for uncertainty. That tells us that the long end will have to settle higher to compensate for the pricing power lost to the re-emergence of inflation in the United States. The Gaza-Israel Conflict will only exacerbate yields in the near term as inflation expectations could spike in anticipation of higher oil prices. However, the rush to safe haven assets could depress interest rates as well, so we anticipate a volatile fall.

Higher Interest Rates, Stronger Dollar

Interest Rate Parity is the notion that, all else equal, if interest rates go up in one country, the exchange rate will adjust to make interest rate investments in the two countries roughly equivalent. As the dollar strengthens, investments in the U.S. will outperform investments abroad, and since May international investments have indeed lagged U.S. investments with the unique exception of Japan. We expect that as the long end of the yield curve continues to adjust higher, the dollar will continue to trend higher and U.S. markets will continue to outperform international markets. The rush to safe haven assets supports this trade as well.

The Fed Reaction to the Gaza-Israel Conflict

The shocking news out of Israel over the weekend could have lasting repercussions on the equity market outlook. First, with oil prices already under pressure from Saudi and Russian supply constraints, energy’s contribution to inflation sets up the Fed to potentially remain hawkish. If that is the case, the outlook for risk assets does not look good. However, if the oil shock goes from a temporary price reaction to an all-out embargo, the hit to the real economy could be massively negative and could force the Fed to cut more than anticipate, but the earnings outlook would be shredded in the wake of the recession that would be kicked off. It feels like a lose-lose situation for the Fed at a time when liquidity and financial conditions are tighter than they have been in over a decade. The resulting volatility could be significant.

Net View

Though we are now cautious on risk assets, in light of the Gaza-Israel Conflict, within Equity we continue to favor U.S. equities over international equities as the dollar continues to strengthen. Within the U.S. equities, large caps stocks look more attractive in a slowdown. Within international equities, Japan continues to look more attractive than Europe and Emerging Markets equities are least attractive.