As the economy continues to show more signs of slowing, the Fed has opted to pause it's campaign of rate hikes.

The Fed Two Step: Summary

- The latest inflation print offers justification for an end to the Fed hikes though the Fed’s tone remains hawkish: Though inflation remains stubbornly higher than the 2% Fed target, it is cooling enough to support more than a pause in the Fed hikes if the economy continues to weaken in June.

- A mild recession is still in the cards with a long, slow recovery: this period of tepid growth will likely usher in continued repricing in the equity markets as interest rates normalize higher and inflation lingers.

- Wage growth normalization remains key to the mild recession outlook: Continued recovery in wages in the U.S. will support consumption, which will support earnings and corporate credit quality.

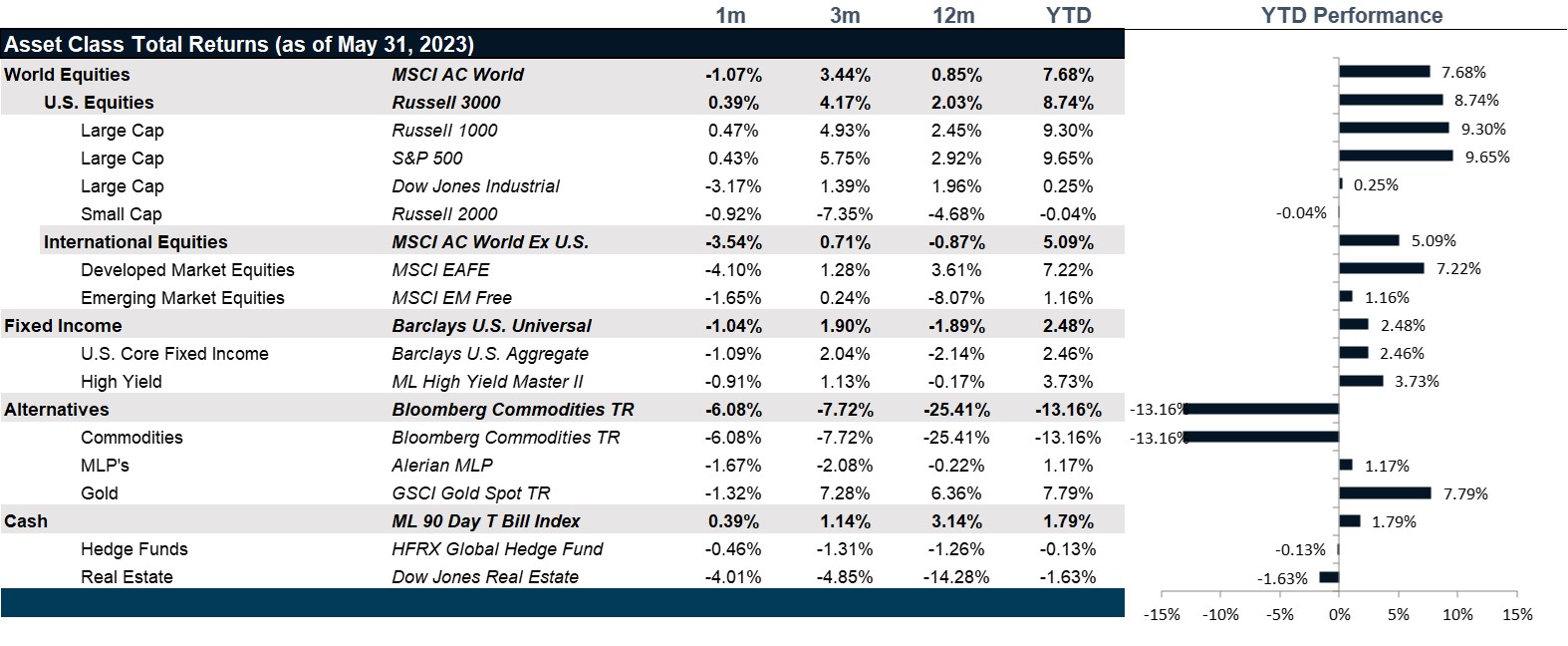

Market Performance as of May 31, 2023

Market Review: Slowing

Equity markets in May were mixed but resilient with the debt ceiling impasse between the Republicans and Democrats taking center stage. The S&P ended the month up 0.4% with large cap stocks continuing to outperform the others. The Dow Jones posted a negative 3.2% return, however the NASDAQ gained 6.9% with the NASDAQ 100 putting on 7.7%. Technology was one of the three sectors that posted gains this month, largely outperforming every other sector with the focus on AI driving gains in the semiconductor space. Communication services and consumer discretionary also posted gains with energy lagging. Inflation remained stubborn with year-over-year at 4.9%, personal spending came in at 0.8% month-over-month much higher than the forecasted 0.4% indicating that consumer spending remained resilient powered by high wages and a strong labor market. The Fed further hiked rates by 25 bps to 5.25% with the Fed Chair Powell mentioning that future rate hikes could be paused, however there were no plans of a rate cut soon. The economy also added 339,000 jobs, however unemployment jumped by 0.3% to 3.7%.

European markets had a dismal month with the STOXX 600 falling 5.8% in dollar terms in May with signs of a global economic slowdown adding to debt ceiling concerns. Inflation in the region remained steady at 7% year-over-year driven by energy prices. In addition, the European Central Bank raised interest rates by 25 bps to 3.25% with the market expecting two more rate hikes. The UK’s FTSE 100 hit a two month low ending the month down 6.5% in dollar terms. Inflation in the UK dropped to 8.7% from 10.1% but remained well above target prompting the Bank of England to further hike rates by 25 bps to 4.5%. Japanese stocks had a strong month with the returning 0.9% in dollar terms return for the month. The Japanese economy remained strong with GDP rising by 1.3% year-over-year for the first quarter, however inflation rose to 4.1%, a historically high level.

Stocks in emerging markets had another disappointing month with the MSCI EM Index returning -1.7% for the month. The Chinese economy showed signs of a recovery but was much weaker than expected. Escalating China-U.S. relations and uncertainty around the U.S. debt deal further weakened investor confidence.

Yields on bonds rose amidst the debt ceiling impasse with the 1-month U.S. treasury surging to 5.28% and the 10- year to 3.64% with the yield curve remaining largely inverted. The 3-month and 6-month yields further increased to 5.52% and 5.56% respectively. Global bonds returned -2% while U.S. bonds were down -1.1%. Gilt ended the month poorly too with the Bloomberg Barclays UK Aggregate Index down -2.9%. However, Euro Bonds posted small gains with the Bloomberg Barclays Euro Aggregate Index gaining 0.4% as some regions in the Eurozone reported better than expected inflation numbers.

The commodity markets performed poorly with the Bloomberg Commodity Index losing -6.1%. Industrial metals also witnessed a decline as a result of reduced global demand for goods and weakening of factory activity in China. The WTI crude landed at around $68 a barrel, down almost 40% from this time last year. OPEC plans to cut production which could spark volatility and drive oil prices up in June. The dollar gained almost 2.5% after almost two months in the red after a resilient labor market and stubborn inflation could indicate another rate hike.

Going Forward: The Fed Two Step

Alas, we can finally see the light at the end of the tunnel for interest rates. With a June pause largely expected, the markets must now consider the likelihood of a July hike, which is still priced into the markets. Beyond that, markets must consider inflation, which continues to show signs of cooling, but could be impacted by the Saudi cut in oil production. And, finally, global growth is continuing to decelerate as the probability of recession is now at 65% with economist consensus forecasts projecting very modest growth in the current quarter, followed by negative growth in Q3 and Q4 of this year and recovering to modest growth in Q1 of 2024. The remainder of 2024, however, is expected to remain below 2%, which although not technically a recession, will not have the feeling of a normal recovery. Though equity markets have reset, the continued pressure of higher-than-normal inflation will continue to put pressure on margins while the tepid outlook for growth will put pressure on revenues and the continued tightening liquidity will put pressure on multiples. Meanwhile, although the debt markets quickly and painfully reset to the new higher rate interest rate regime, the persistence of the inverted yield curve continues to be unsustainable.

The Fed vs. Inflation

Reading into the May inflation report, we see energy as a large detractor from headline CPI, which grew at 4.05% year over year while food prices continued to grow by less. Meanwhile core inflation grew by 5.33% with both components showing signs of cooling. Goods prices continue to fall while services prices, by far the largest contributor to inflation, also showed some signs of cooling. Median wage growth continues to fall but remains stubbornly high at 6% largely resulting from labor market shortages. That said, the duration of unemployment finally rose to 21 weeks, though still low, at least demonstrates to the Fed that policy is finally beginning to bite. This could open the door for more than a pause. The data could support an end to the Fed’s tightening campaign, which is currently not priced into the fed Fund’s Futures markets. In fact, the hawkishness of the Fed’s tone suggests that it will take further evidence of economic weakening before the Fed completes the rate hikes.

Global Growth

With inflation higher than it has been in four decades and unemployment lower than it has been in more than five decades and interest rates rising at the fastest pace in recent history, the outlook for global growth outlook is not so clear. We see clear signs of deceleration in the U.S. and Europe while China continues to re-open and Japan continues to surprise to the upside. The tightening of financial conditions kicked off by the failure of SVB followed by the takeover of Credit Suisse remains a point of weakness in the outlook as many economists see further potential for liquidity disruptions, despite the overall solvency of bank balance sheets.

Valuation

Despite the dramatic reset in the debt markets and the volatility in the equity markets, the markets have not yet fully priced in lower margins that must come from persistently higher inflation as globalization slows and aging demographics combined with low birth rates conspire to reduce the supply of available workers. Nor have they priced in lower multiples that must arise from higher interest rates and tighter lending conditions. Though lending conditions will moderate, interest rates are expected to normalize at a higher rate in order to remain in positive real territory if inflation remains high. Part of the normalization of data includes the normalization of wage growth which is making up for over a decade of compression. The good news on this front is that revenues should be supported by continued consumption capability in a world of positive real wage growth that is above the growth in inflation. This support can and should also support the outlook for credit defaults. Though credit downgrades still outpace upgrades, the pace is already slowing as companies continue to perform on their debt obligations. Though there will undoubtedly be some volatility as companies adjust to higher interest expenses, we do not expect mass insolvency among investment grade credits. However, smaller companies and lower grade debt may be in for some turbulence over the next year, making issuer selection extremely important.

Net View

We remain balanced in our outlook with upside risks equal to downside risks in the portfolio.