Recession risks continue to rise.

A Roadmap for 2023: Summary

- Stock picking will matter in 2023: With interest rates expected to normalize at higher levels, we expect valuations will fall and stock-specific resilience will matter to portfolio performance.

- Yields on high-quality debt remain attractive: With recession risk on the table for 2023, high-grade corporate debt remains attractive, with significantly less risk than equities.

- The outlook for 2023 has some downside risk: If labor shortages persist and wage inflation continues, the Fed may be forced to go beyond what is priced in, which could herald a deeper impact on housing prices, a major source of wealth and stability for U.S. households.

You can read the full Market Update below.

Market Review: A Brief Moment of Optimism

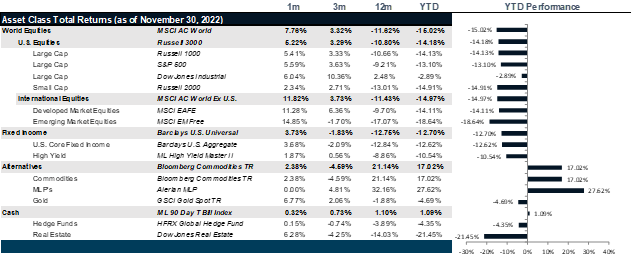

U.S. markets had a positive month in November, with the S&P 500 ending the month up 5.6%, the Dow Jones up 6.4% and the NASDAQ up 4.5%, though the markets gave back some of those gains at the start of December. November’s inflation print looked to be peak inflation. When the Fed chair indicated that rate hikes could be less aggressive, investors responded positively to this news. Markets witnessed one of their best single-day rallies in two years after year-over-year inflation came in at 7.7%, a lower-than-expected number. The materials and industrials sectors paved the way with the most gains; however, all sectors had a positive month. The U.S. economy added 263,000 jobs in November, beating market forecasts, but the number of jobs added was still lower than in October. The high interest rates, however, are causing a slump in the housing market as the extraordinarily high mortgage rates are dissuading potential home buyers. All that said, the Fed has remained hawkish, particularly after the strong consumption data, taking some of the wind out of the sails.

European stocks continued their gains from October. With eurozone inflation easing to 10% from 10.6% in October, there is hope that inflation has peaked even though inflation in the UK rose to 11.1%. The Bank of England responded by raising interest rates by 25 basis points to 3%, the highest the country has seen since the Global Financial Crisis of 2008. UK equities, however, had a good month, as investors are still positive about the new government and there is hope that the economy is stabilizing. With Europe experiencing milder weather, the energy crisis has eased as demand has reduced and the risk of running out of gas has also further reduced. However, energy prices remain a primary driver of inflation. Japanese markets had a good month as well, with the yen strengthening against the U.S. dollar, reversing a trend it has set all year. However, Japanese inflation numbers are still high, with the CPI rising further to 3.7%.

Emerging markets recouped their losses from October, outperforming developed markets, with China leading the pack. Markets were optimistic about China relaxing COVID-19 regulations and about the meeting of U.S. President Joe Biden and Chinese Premier Xi Jinping signaling an ease in tensions between the two countries. Other Asian markets performed well, too, on the backdrop of the dollar weakening and signs that the Fed was starting to ease rate hikes in the U.S. Strong gains were noticed in Malaysia, South Korea, the Philippines and Singapore.

The U.S. bond market also registered a good month with a significant drop in yields. The U.S. 10-year yield dropped to 3.61% from 4.05%, and the two-year yield dropped to 4.31% from 4.49%. However, the yield curve inversion widened to more than 80 basis points, signaling continued high expectations for a recession. Global bond markets are behaving similarly, with the long end falling, driving down yields and pushing up bond prices. The Bloomberg Global Aggregate Bond index was up 4.7%, its best month since the Global Financial Crisis.

The commodities market had a bad month, with energy the worst performer. Industrial and precious metals made gains but were offset by the huge losses in the energy and agriculture sectors. Silver prices rose significantly, with a lot of demand from automakers and the solar industry. Crude oil wiped most of its gains from this year, with West Texas Intermediate futures settling close to $77 a barrel. Crypto markets had an ugly November, with the FTX collapse being the talking point all month.

Figure 1: Market Performance as of November 30, 2022

Going Forward: A Roadmap for 2023

As we come to the end of 2022, it is likely that we will look back on this year as the end of an era of excess liquidity and a pivot point. That pivot is not yet complete. If 2022 was the year of the pivot, then 2023 will be the year of the wobble, much like when many objects wobble before settling. We see shifts on several fronts that will lay the path we are about to embark on. Financial conditions and liquidity are set to change, possibly for a long time to come, and along with that, risk appetite and valuations. In addition, globalization and the supply chain will probably never be the same after the pandemic, which will have long-lasting effects on inflation, labor markets and the dollar. Finally, demographics, the long-sleeping bear, may awaken and wreak havoc on best-laid plans.

Financial Conditions and Liquidity

Expectations for the fed funds rate, the rate at which banks borrow from one another and the rate set by Federal Reserve policy, is expected to rise to a peak of 5%, a level not seen since before the Great Financial Crisis. And, though still low by 1980s standards, it is a level that will have lasting implications for some segments of housing prices as it feeds through to mortgage rates, which are currently at 20-year highs, as well as into rental rates, which rose rapidly in response, year over year, according to the Zillow Rent Index. And, while housing prices are supported by a lack of inventory, which keeps the fall from being either quick or precipitous, equity pricing, on the other hand, has been fast and furious in terms of repricing. Companies with no earnings have been decimated, and defensive companies have been overbought. The road to equity survival will be one fraught with land mines between the near term and the long term, where near-term pain may be too great to hold until the long-term stories kick in. Bonds, on the other hand, have repriced quickly and are now set to be an active participant in the portfolio return for the first time in a very long time. After booking the worst returns in decades, returns are starting to perk up as the Fed nears the end of its hiking cycle. And newer entrants into the bond markets can now enjoy 4.3% yields on broad investment grade debt, 5% yields on U.S. investment grade corporates and 8.6% yields on U.S. high-yield debt. As we stare a potential recession in the face, these yields are very attractive, particularly in the investment grade arena, where downgrade activity is still somewhat subdued.

Globalization and the Supply Chain

Last-mile delivery is now more likely to come at the end of a shorter journey as the nation rethinks its dependence on China and offshore manufacturing and services. While we have exported inflation and imported deflation for the better part of three decades, we are finally at the end of that margin expansion. As we start to nearshore and onshore key components of our supply chain, the ultimate impact will be inflationary, at least in the short term, though we should say that it will be the most productive form of inflation – wage inflation, which drives economic consumption and growth. This is the kind of inflation that monetary policy was created to combat. And, though it will almost certainly herald higher interest rates for some time to come, it will also mean a wealthier U.S. middle class and better risk allocation and risk/return trade-offs. So, we expect that valuations will be lower, but actual real values could likely be significantly higher. The great risk to this outlook is the potential for isolationist behavior on the geopolitical front, which could lead to a higher level of security and social risk.

Demographics

We have long discussed the Great Resignation, which has led to strong labor markets in the face of a determined Federal Reserve, primarily because older workers have resigned, leaving a dramatic shortage of workers in the labor market. And, looking at the demographics of the U.S., this trend is only likely to increase, with fertility rates dropping and immigration mired in political red tape. While the fewer left in the workforce are very likely to be paid more, the pressure to automate will increase and the buying power of retired workers will continue to be eroded. Moreover, if the U.S. is serious about reducing dependence on Chinese manufacturing, the sheer number of workers required to manufacture the goods demanded by the insatiable U.S. consumer is massive. The total number of people employed in the manufacturing sector in China is about 100 million workers, compared with less than 20 million in the U.S. With the labor market in shortage and likely to remain so through 2023, we can expect some aspects of wage growth to continue to remain high absent a change to immigration trends, keeping inflation higher for longer and making consumption challenging. The offset to this would be a change in immigration trends, which could add to the labor market to ease the pressure on wages, though for the moment, that does not look likely.

Net View

While we continue to play defense with U.S. equities, we anticipate that when the Fed does finally reach its peak, the more resilient segment of the growth market could start to come back. 2023 will be another year for stock picking rather than for passive investing. Yields still favor high-grade credit and broad high-grade debt generally.