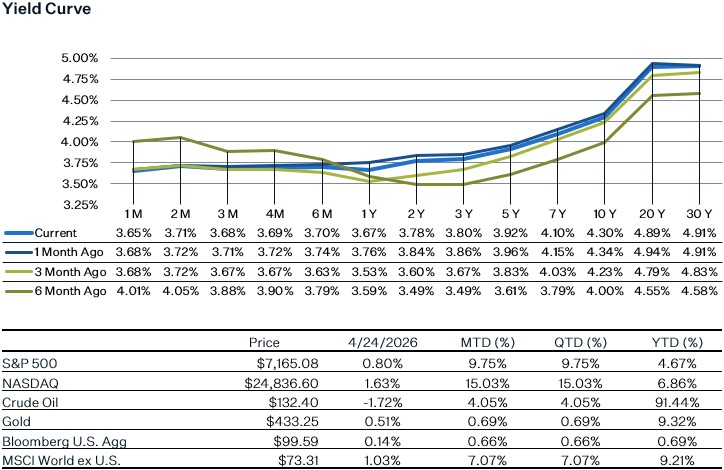

Market Update

U.S. equity markets ended the week slightly higher, as strong corporate earnings were a tailwind to markets while the uncertainty around the war likely kept returns modest. The prolonged extension to the ceasefire between U.S. and Iran has reduced the near-term risk of conflict resumption, however, oil inventories continued to be drawn down as tankers remain unable to transit the Strait. Should the disruption persist, a sharper risk emerges if inventories approach operational minimums, the market transitions from a price shock to a physical shortage, sending prices sharply higher. Due to strong earnings, the Nasdaq and the S&P 500 set new records last week, with semiconductors being the biggest beneficiaries rallying over 18 days driven by AI. The Q1 earnings growth rate for the S&P 500 is coming in at 15.1% right now, above the 13.2% estimate before the quarter ended. Roughly a third of companies that have reported have beat estimates and the earnings upside surprise is roughly 13%. Last week we had the retail sales data for March, which came in above expectations although most of the monthly increase came from higher gas prices. This week we have the FOMC meeting on Wednesday and the PCE data out on Thursday. We also have most of the Mag 7 reporting including GOOGL, AMZN, MSFT, META, and AAPL. Investors will likely be closely dissecting AI capex spending expectations and hoping for early signs of AI efficiency gains.

Retail Sales

Retail sales for March came in above estimates, increasing 1.7% month-over-month although the majority of the gain came from higher gas prices as increases in gas station sales surged 15.5%. Excluding gas sales, retail sales rose 0.6% in March, which is still a solid gain for the month. This is likely due to tax refunds that offset the gasoline price increases, enabling consumers to still engage in healthy spending elsewhere. Besides spending on gas, spending was healthy in categories such as furniture/home stores (+2.2%), general merchandise stores (+1.0%), and online stores (+1.0%). One category that has seen weakness in the past few months is spending on food services or restaurants/bars. Restaurant/bars spending was basically flat for the month, along with apparel and sporting goods stores. While this retail sales figure suggests that consumers haven’t pulled back since the start of the war, the tax refunds could be masking some underlying weakness, thus it will be important to keep an eye on the sales data in the coming months.

Summary of Kevin Warsh’s Current Views

- Framework Overhaul: He argued that the current Fed analytical models are broken specifically citing the 2021–2022 transitory inflation misstep as proof. He wants to move and toward a more data-dependent, reactionary stance.

- Narrow the Mandate: Warsh believes the fed should focus on price stability and maximum employment while vocalizing opposition to the Fed’s involvement in climate risk or social policy.

- The AI Productivity: He has suggested that if AI-driven productivity gains are real, the economy can support a higher growth rate without triggering inflation, which might allow for lower neutral rates than traditional models suggest.

- Trimmed Mean & Median Inflation: Warsh explicitly stated he prefers the Dallas Fed Trimmed Mean PCE over the standard Core PCE because Core PCE removes only Food and Energy, Trimmed dynamically removes the most extreme price changes in any given month thus filtering the noise. Currently, Core PCE is stuck at approximately 3%, but Trimmed Mean has hit the 2% target. By switching, Warsh can technically claim mission accomplished on inflation to justify rate cuts.

US Flash April PMI

The headline US Flash PMI rose from 50.3 in March to 52.0 in April of this year, led by strength in Manufacturing, while service somewhat moderated the figure. At first glance, the Manufacturing PMI figure might paint a rosy outlook, as it came in at its highest level in nearly 4 years and the index came well above expectations at 54.0, versus a 52.9 forecast. Yet, looking under the hood, the print appears to be artificially driven by a panic amongst businesses to lock in their orders now before further supply chain disruptions occur, not by a genuine surge in demand. Stresses in the supply chain are being felt broadly, as current delivery times have reached their highest levels since August 2022, and higher input costs are forcing some businesses to pass on higher prices to consumers. Meanwhile, the service index also beat expectations, coming in at 51.3 versus the expected 51.0, but the hiring slowdown was noticeable as employers hesitated to add headcount due to uncertainty about future demand and high input costs limiting hiring opportunities. Inflation appears to be temporarily resurgent, with ongoing supply disruptions pushing input costs to their highest levels in 11 months, and the average prices charged for goods and services increasing at the fastest rate since July 2022. Overall, the report shows an economy that on the surface appears to be resilient amid the ongoing Middle East conflict, yet the underlying drivers are short-term and, over the long term, could actually be detrimental. Moving ahead, the Federal Reserve is likely to continue focusing on the labor market, especially on how AI is impacting employee prospects, but the potential for inflation to reignite will make some FOMC members uneasy about rate cuts, particularly given the scar tissue from 2022-2023.

Sources:

https://www.pmi.spglobal.com/Public/Home/PressRelease/8bdf1bb2dddf420e9c0e9d7e22f75c09

https://insight.factset.com/sp-500-earnings-season-update-april-24-2026

https://markets.jpmorgan.com/jpmm/research.article_page?action=open&doc=GPS-5278063-0

https://www.census.gov/retail/marts/www/marts_current.pdf